Car Transport Payment Processing: Deposit on a Card, Balance on Delivery

A Car Ships on a Card Deposit and a Cash Balance

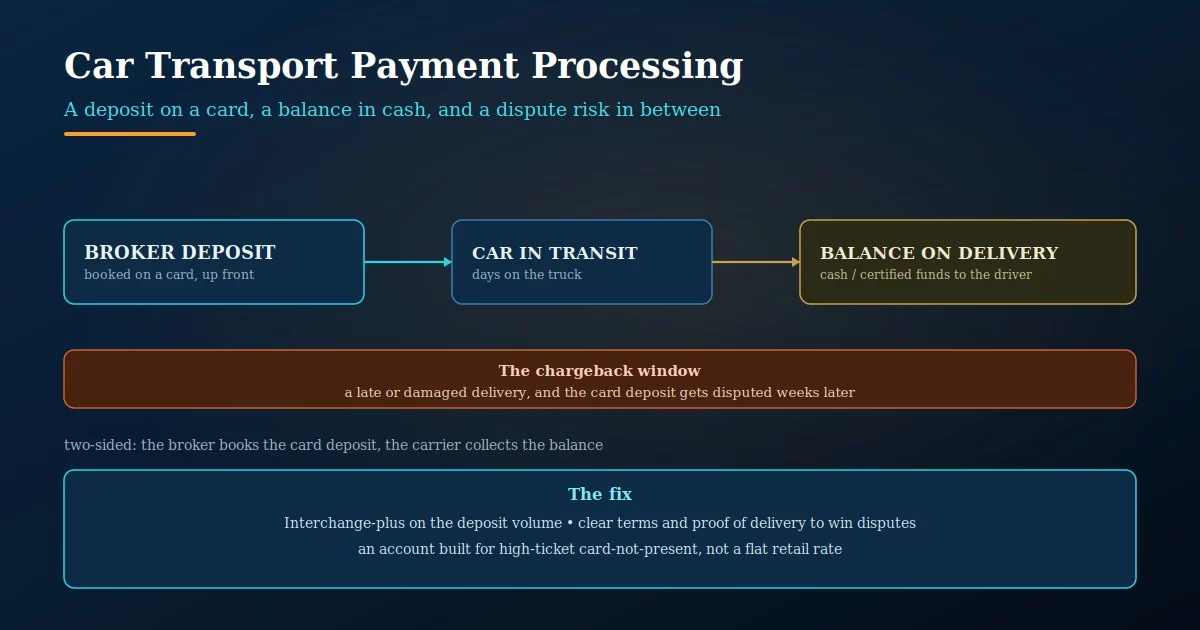

Moving a vehicle across the country doesn’t get paid like a normal sale. The customer puts a deposit on a card when they book — often a few hundred dollars against a thousand-dollar-plus move — and the balance is paid in cash or certified funds directly to the driver when the car is delivered. That split is the whole shape of car transport payment processing: the card touches the deposit and nothing else, and the deposit is exactly where the trouble lives.

Because the deposit is a high-ticket, card-not-present charge taken days or weeks before anything is delivered, it carries a kind of risk most businesses never face — the customer can dispute it long after they’ve paid it, if the move goes the way auto transport moves often do. Get the pricing on that deposit right and the dispute exposure managed, and you’ve handled almost everything that matters.

The Card Touches the Deposit, Not the Move

It’s worth being precise about what actually runs on a card, because it’s narrower than people assume. The deposit — the broker’s fee, or a partial against the total — is booked on a card at the time of reservation, card-not-present, over the phone or through a web form. The balance, the larger share, is collected on delivery in cash or certified funds handed to the carrier. So your card volume isn’t the value of the moves you book; it’s the stack of deposits, each a sizable card-not-present charge taken up front. For car shipping payment processing, that distinction is the whole ballgame.

That matters for pricing because card-not-present, high-ticket transactions don’t belong on a flat rate built for swiped retail sales. A deposit keyed in days before delivery is priced differently from a card tapped at a counter, and a processor selling you a one-size retail rate is mispricing the only transactions you actually run. Sound car transport payment processing starts by treating the deposit as what it is: high-ticket, card-not-present, and the entirety of your card business.

Booking $200,000 of vehicle moves a month doesn’t mean $200,000 of card volume — it means the sum of the deposits, because the balances come in as cash on delivery. Price around that reality: a book of high-ticket, card-not-present deposits, not the headline value of the freight.

Brokers Book the Card; Carriers Collect the Cash

Auto transport is a two-sided trade, and which side you’re on determines what your payment setup even needs to do. Brokers arrange the move, match it to a carrier, and take the card deposit — so for a broker, the deposit is the card business, full stop. Carriers are the truckers who actually haul the vehicles and collect the cash balance on delivery; their card exposure is smaller and different. Most companies marketing “car shipping” to the public are brokers, which means for most of this industry, auto transport payment processing is really about handling that book of upfront card deposits cleanly.

Knowing which side you sit on keeps you from buying the wrong setup. A broker needs a car transport merchant account tuned for high-ticket card-not-present deposits and the disputes that come with them; a carrier collecting mostly cash needs far less. The mistake is a broker treating its deposit book like incidental card volume when it’s the financial core of the operation.

If you’re a broker, the deposit book is your card business and deserves pricing and dispute tooling built for it. If you’re a carrier collecting cash on delivery, your card needs are lighter. Buying the wrong setup — or a generic retail one — means paying for what you don’t use while mispricing what you do.

A Late Delivery Becomes a Disputed Deposit

Here’s why the deposit is more than a pricing question. Auto transport runs late — drivers get delayed by weather, routing, breakdowns, and loads that fall through, and a pickup window that slips by days is routine, not exceptional. When a move runs late or a vehicle shows up with a scratch, the customer’s instinct is to dispute the card deposit they paid weeks earlier, and a card-not-present deposit taken long before delivery is one of the easier charges in the world to challenge. A run of those disputes is what pushes a processor to reclassify a transport company as high-risk, with rolling reserves attached.

The defense isn’t luck, it’s documentation. Clear written terms the customer agrees to at booking, realistic delivery windows rather than promises you can’t keep, proof of pickup and delivery condition, and a processor who understands transport disputes instead of freezing your account at the first one. This is the part of car transport payment processing that separates a stable operation from one that lurches between chargeback waves — and it’s almost entirely within your control if the setup is built for it from the start.

A late or imperfect delivery plus a weeks-old card-not-present deposit is the easiest dispute a customer can win — and a cluster of them lands you on a high-risk reserve. Written terms agreed at booking, honest delivery windows, and proof-of-delivery documentation are what let you fight and win those disputes instead of absorbing them.

What Car Transport Payment Processing Should Actually Look Like

The setup follows the two facts that define the business. Price your deposit volume on interchange-plus with an auto transport merchant account built for high-ticket card-not-present charges, not a flat retail rate that misprices the only transactions you run. Build your dispute defense in before you need it — terms agreed at booking, honest windows, proof of delivery — and work with a processor who treats transport chargebacks as a known part of the trade rather than a reason to freeze you. Track your effective rate on the deposit book, since that’s your entire card cost, and know where the high-risk line sits so a bad month of delays doesn’t blindside you.

None of this changes how you book loads or how a driver collects on delivery. It changes whether your deposit book is quietly overpriced and whether a normal run of late deliveries turns into a reserve that chokes your cash flow. For a transport broker, those two things — the rate on the deposits and the handling of the disputes — are the whole payments game.

A flat retail rate on high-ticket card-not-present deposits overcharges every one of them, and no dispute defense means a normal stretch of late deliveries becomes a chargeback wave and a high-risk reserve. Both are avoidable: transparent pricing built for card-not-present, and documented terms plus proof of delivery so disputes get fought, not eaten.

Frequently Asked Questions

Typically a deposit on a card at booking, then the balance in cash or certified funds paid to the driver on delivery. The card transaction is the deposit — a high-ticket, card-not-present charge taken up front — while the larger balance is collected on delivery rather than run through a terminal.

It can be, because card-not-present deposits taken weeks before delivery get disputed when moves run late or vehicles arrive damaged, and a cluster of those chargebacks pushes a processor to reclassify the account. It isn’t automatic — clear booking terms, honest delivery windows, and proof-of-delivery documentation keep many transport brokers on standard pricing.

Usually no — the deposit goes on a card at booking and the balance is collected in cash or certified funds on delivery. That deposit is your card volume, so it’s the thing to price carefully and protect against disputes, rather than trying to push the entire move through the card rails.

Keep reading on automotive payments and what you pay

See What Your Deposit Book Is Really Costing You

Send Brookside one recent statement and we’ll calculate your true effective rate on your card-not-present deposit volume, show you whether a flat retail rate is overcharging it, and check your chargeback exposure before a stretch of late deliveries puts you on a reserve. No switch required to find out. Learn more about payment processing consumer protections from the CFPB.

Get Your Transport Rate ReviewedNo obligation • No pressure • Response within one business day