Country Club Payment Processing: Several Tills, One Member Tab

A Country Club Runs Five Businesses Behind One Gate

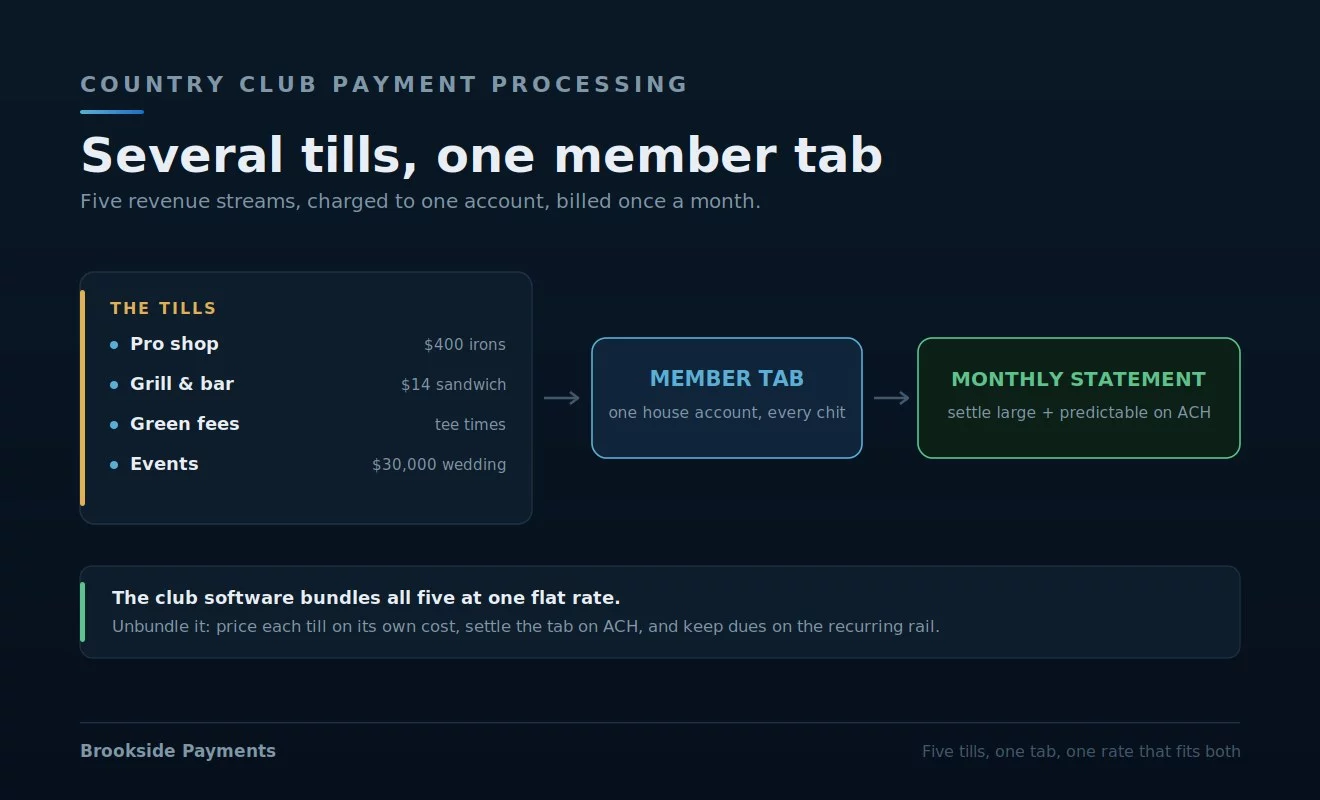

A country club isn’t one business — it’s five running at once: a pro shop, a grill and bar, a golf operation selling green fees and tee times, an events and catering calendar, and a membership office collecting dues. Each is a different kind of transaction, and the club-management software that ties them together — Jonas, Clubessential, Northstar — usually bundles all the card processing too, often acting as the payment facilitator itself, at a flat rate buried inside the platform. That’s the first half of country club payment processing: five revenue streams, one hidden rate.

The second half is the part almost no other business has — the member tab. At a club, members don’t swipe at the grill or the pro shop; they sign a chit and charge it to their account, then settle one monthly statement. That house-account model is the heart of how a club gets paid, and it changes how the processing should be structured. Good country club payment processing has to fit both realities at once: the five tills and the one tab.

One Software Rate Across Five Very Different Tills

The pro shop sells a $400 set of irons. The grill rings a $14 sandwich. The starter collects a green fee. The events office books a $30,000 wedding. Each has a completely different cost profile — and when the club-management platform bundles the processing at one flat rate, every one of them gets charged the same way, hiding where you’re overpaying. Several club platforms act as the payment facilitator, which makes the convenience real but the rate invisible: it never arrives as a processing statement you can shop, because it’s folded into the software bill. That’s the most overlooked line in country club payment processing.

Pulling the rate apart from the platform is usually the biggest single saving in country club payment processing, and it rarely means abandoning the software your staff and members rely on. Many club systems — Jonas, Northstar, Clubessential — integrate with outside processors through supported gateways, so you keep the member management, tee sheet, and POS while routing the actual card processing to an interchange-plus account where the pro shop, the grill, and the events deposit are each priced on their true cost. Sound golf club merchant services separate the platform you run on from the rate you pay through it.

In country club payment processing, club platforms (Jonas, Clubessential, Northstar) bundle card processing — often as the payment facilitator — at one flat rate across a $14 sandwich, a $400 pro-shop sale, a green fee, and a $30,000 event. Most integrate with outside processors through supported gateways, so keep the software and route processing to interchange-plus where each stream is priced on its real cost.

Members Charge It All to One Account — and You Reconcile It

The member tab is what makes a club distinct. A member plays a round, buys a sleeve of balls, has lunch at the turn, and tips the bag staff — and signs for all of it, charging every chit to a house account billed once a month. Almost nothing is a card swipe at the point of sale; it’s an internal charge that rolls up into a member statement. That means country club payment processing is really two systems: the member-billing engine that tracks chits and produces statements, and the actual card or ACH settlement when members pay those monthly bills.

Two things follow. First, reconciliation across pro shop, grill, dues, and events is a genuine workload — controllers describe cutting it from hours to minutes once settlement is consolidated and reported cleanly, so the reporting your setup produces matters as much as the rate. Second, when members settle those monthly statements, the payment that actually touches a card network is large and predictable — exactly the kind of recurring charge that belongs on ACH rather than card rates wherever members will allow it. A country club merchant account built for the tab handles both the chit-level detail and the cheap settlement of the monthly bill.

Members charge chits to a house account billed monthly, so almost nothing is a POS swipe — it’s an internal charge rolled into a statement. Make sure your setup gives clean chit-level reconciliation across every outlet, and when members pay those monthly bills, route the large, predictable payments to ACH rather than card rates where you can.

A $4 Beverage Cart to a $40,000 Wedding

Few businesses span the range a club does in a day: a four-dollar drink from the beverage cart, a green fee, a few hundred in the pro shop, a catered member event, and a wedding worth tens of thousands booked a year out. Each end carries different economics. The high-volume, low-ticket food-and-beverage side lives and dies on gratuity handling — tips added after the check, done poorly, cause adjustment downgrades that quietly raise your rate. The pro shop benefits from level-2 and level-3 data on corporate and member cards. And the events side behaves like a venue: large deposits taken far in advance, with the hold and refund exposure that comes with them. Country club payment processing has to be underwritten and equipped for the whole spread, not the average chit.

That’s why a single flat rate fails a club so badly — it ignores the gratuity mechanics of the grill, the data rates available in the pro shop, and the deposit profile of the events calendar, and prices them all as if they were identical. The events deposits in particular deserve the same care a banquet hall gives them, since money collected a year before a wedding is exactly what triggers a processor hold. Seasonal swing compounds it: in a seasonal climate, card volume peaks in summer while dues and fixed fees run all twelve months. Thorough golf course payment processing prices each stream on its own terms.

A club ranges from a $4 cart drink to a $40,000 wedding. The grill needs clean gratuity handling so tip adjustments don’t downgrade transactions; the pro shop benefits from level-2/level-3 data; events behave like a venue, with large advance deposits that can trigger holds. In country club payment processing, price each stream on its own terms, and account for the seasonal swing against year-round dues.

Keep the Platform, Price Each Stream, Bill the Member Cleanly

The fix for a club pulls the threads together: keep the club-management platform your members and staff know, but route the card processing through it to a transparent interchange-plus account so the pro shop, grill, green fees, and event deposits are each priced on their real cost. Handle the grill’s gratuity cleanly, capture level-2/level-3 data where it helps, and treat large event deposits with venue-grade care. Settle the monthly member statements on the cheapest rail — ACH wherever members allow — and keep the chit-level reconciliation tight. Recurring monthly dues are their own discipline, worth handling the way any recurring membership billing should be priced. That’s what turns country club payment processing from a bundled flat rate into a setup that fits the club.

Keep the platform; route processing to interchange-plus so each stream is priced on real cost. Handle grill gratuity and pro-shop level-2/level-3 data, treat event deposits like a venue would, settle monthly member statements on ACH where possible, and keep chit-level reconciliation clean. Dues ride the recurring rail. In country club payment processing, one flat rate fits none of it.

Five Tills, One Tab, One Rate That Should Fit Both

A country club loses money in the seams between its businesses — five revenue streams charged one flat bundled rate, a member-billing system only as good as its reconciliation, gratuity and event deposits handled like ordinary retail, and dues priced as an afterthought. Country club payment processing done well closes those seams: unbundle the processing from the club software so each stream is priced right, build for the member tab and its reconciliation, settle the monthly statement cheaply, and give events and dues the handling they each need. Keep the clubhouse running on the platform it knows; just make sure the rate underneath fits all five tills and the one tab.

Frequently Asked Questions

Because a club is several businesses at once — pro shop, grill, golf, events, and membership — and members charge most of it to a house account billed monthly rather than swiping at the point of sale. A standard retail account is built for one kind of transaction, not five, and it has no concept of the member tab, the chit-level reconciliation, or the recurring dues that define how a club actually gets paid.

Usually not. Platforms like Jonas, Clubessential, and Northstar integrate with outside processors through supported gateways, so you can keep the member management, tee sheet, and POS while routing the actual card processing to a transparent interchange-plus account. In country club payment processing, the bundled rate inside the software — often charged because the platform acts as the payment facilitator — is typically the most expensive and least visible part, and unbundling it is usually the biggest saving.

Differently. In country club payment processing, recurring monthly dues are large, predictable, repeating charges that belong on ACH or a recurring rail priced like any membership billing, not on full card rates. The pro shop, grill, green fees, and events each have their own economics — gratuity handling, level-2/level-3 data, event deposits — and should be priced on interchange-plus so each stream reflects its real cost rather than one flat number across all of them.

Keep reading on multi-stream, member, and event billing

Get Your Whole Club Priced, Not Just the Average

Send Brookside one recent statement — or your club platform’s payments summary — and we’ll break out your true effective rate across the pro shop, grill, golf, and events, show what’s hidden inside a bundled or payment-facilitator rate, and flag whether moving member-statement settlement and dues to ACH would save. This is golf course credit card processing priced on what each stream actually costs. Keep the platform; we’ll fix the rate underneath. You can also review card payment protections from the CFPB.

Get Your Club ReviewedNo obligation • No pressure • Response within one business day