Auto Dealer Payment Processing: The Car Can’t Go on a Card

At a Dealership, the Biggest Sale Is the One That Never Touches a Card

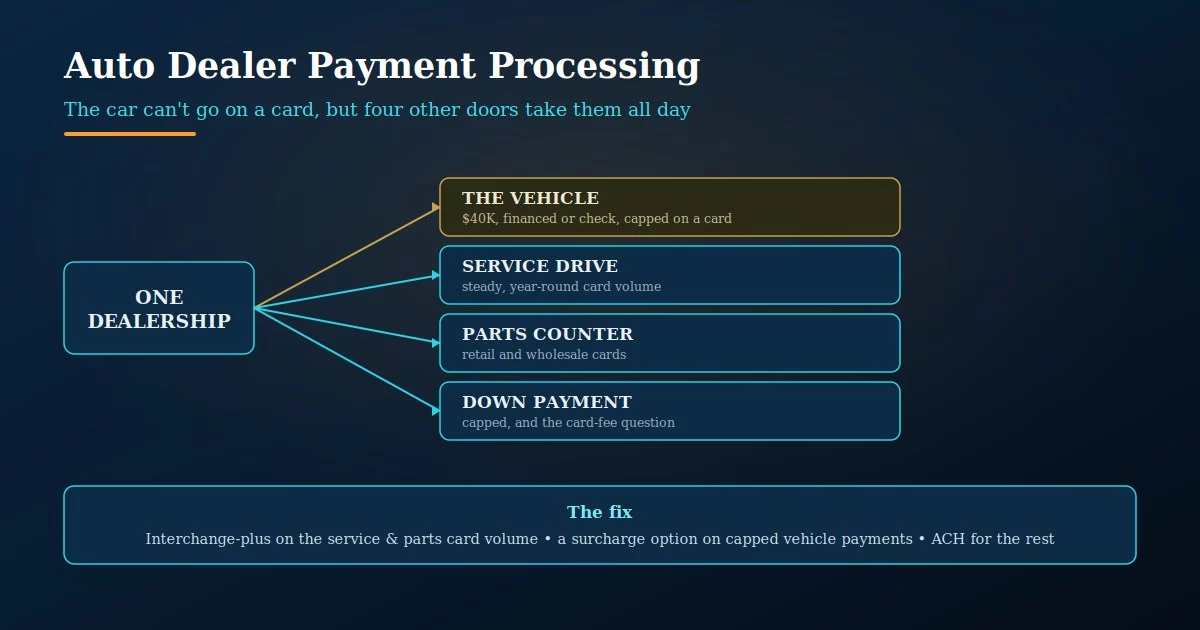

A car dealership is four or five businesses sharing a lot. There’s the vehicle sale, the service drive, the parts counter, the finance office, and the used side — and they don’t move money the same way at all. The mistake in auto dealer payment processing is treating the dealership as one account on one rate, when the single largest number on the floor — the car itself — is the one piece that mostly never runs on a card.

Get that backwards and you lose money twice: you set up your processing around the vehicle sale that barely uses cards, and you under-manage the service drive and parts counter, where cards actually run all day, every day. The card business at a dealership is real and steady, which is why an auto dealer merchant account should be built around the service drive, not the showroom. It’s just not where the marquee number is.

Why the Car Can’t Go on a Card

Run a $40,000 vehicle on a credit card and the interchange alone is somewhere north of a thousand dollars — often more than the dealership’s margin on the unit. No dealer absorbs that, which is why almost every store caps card payments on the vehicle itself, commonly at a few thousand dollars, and routes the rest through financing, a check, or a bank transfer. The car is a financed or cash transaction with a small card slice on top, not a card sale.

That cap is the right instinct, but it’s usually set once and never revisited, and it interacts with the rest of the setup in ways that cost money. The question isn’t whether to cap — it’s what to do with the capped slice you do accept, and whether the much larger card volume in the rest of the store is priced as carefully, which is what auto dealer payment processing is really about.

At roughly 2% to 3% all-in, a card-run vehicle sale costs more in processing than most units earn in gross. That’s why the cap exists everywhere. The point isn’t to fight it — it’s to recognize that since the vehicle isn’t your card business, your processing setup shouldn’t be built around it.

The Service Drive Is Your Real Card Business

Walk past the showroom to the service drive and you find the dealership’s true card volume: repairs, maintenance, diagnostics, tires — ticket after ticket, all year, in amounts that run on cards without a second thought. For most stores the service department processes far more card transactions than the sales floor ever will, and because it’s steady and unglamorous, it’s also the volume nobody negotiates the rate on. A strong car dealership payment processing setup prices the service drive like the real card business it is.

The parts counter is the same story with a twist: it sells retail to walk-ins and wholesale to other shops, so it carries both ordinary card volume and commercial-card transactions that can qualify for lower interchange when the right data is passed. Between service and parts, a dealership runs serious card volume every day — and if all of it sits on one flat rate set around the showroom, the markup on that steady stream is the single most overlooked cost in dealership credit card processing.

The service drive and parts counter run cards every day at predictable amounts — that’s your card business, and it belongs on interchange-plus so the markup is visible. Most dealers negotiate hard on the car and never look at the rate running through the back of the store, which is exactly backwards.

What to Do With the Card Payments You Do Take Up Front

Then there’s the down payment and the capped portion of the vehicle a customer wants to put on a card — for the points, for the float, for whatever reason. This is real card volume at large ticket sizes, and it’s where the surcharge-or-absorb decision actually matters. Some dealers add a compliant surcharge to card payments on the big-ticket items so the cost is carried by the customer who chose the card; others fold a modest cap into the deal. Either way it’s a deliberate choice, not a default, and the rules around surcharging vary, so it’s worth setting up correctly as part of your car dealership merchant services rather than improvising at the desk.

F&I products — service contracts, GAP, warranties — mostly ride along with the financing rather than the card rails, so they’re rarely the card question. The card question up front is narrow and specific: the down payment and the capped vehicle slice, and whether the customer or the store carries the cost of running them.

A down payment or capped vehicle payment on a card is large enough that who absorbs the fee actually matters. Surcharging the customer who chose the card, where it’s done compliantly, keeps that cost off the store — but it has to be set up deliberately, because the rules differ and a sloppy surcharge causes more problems than it solves.

What Auto Dealer Payment Processing Should Actually Look Like

Good auto dealer payment processing stops treating the dealership as one account and prices each door to its reality. Put the service drive and parts counter — your real, steady card volume — on interchange-plus so the markup on every repair ticket is visible instead of buried. Pass the right commercial-card data on wholesale parts so those transactions earn their lower interchange. Make a deliberate choice on the capped vehicle and down-payment card slice — surcharge it compliantly or cap it, but decide. Keep the financed vehicle where it belongs, off the card rails. And track a blended effective rate per department, because a single store-wide number hides which door is leaking.

A dealership that does this stops overpaying on the thousands of small card tickets that actually make up its card volume, and stops accidentally eating interchange on the big payments it should have surcharged or capped. The car was never the card business. Once the setup reflects that, the money that was quietly leaking out of the service drive stays in the store.

One flat rate across the whole store is the costliest setup a dealer can run: it overcharges the steady service-and-parts card volume because the markup is hidden, and it leaves the big-ticket card payments unmanaged so the store eats interchange it could have surcharged. Price the doors separately — the service drive on interchange-plus, the big tickets by deliberate choice.

Frequently Asked Questions

Usually only up to a cap — commonly a few thousand dollars — with the rest financed or paid by check. Running a full vehicle on a card would cost the dealer more in interchange than the unit earns in gross, so nearly every store limits it. Some dealers allow more if the card cost is surcharged to the buyer.

The service drive and parts counter, not the showroom. Repairs, maintenance, and parts run on cards all day at predictable ticket sizes, and for most stores that’s far more card volume than vehicle sales. It’s also the volume nobody negotiates the rate on, which is why it’s where the markup hides.

It’s a real option on the big-ticket card payments — the down payment and capped vehicle slice — where the fee is large enough to matter, provided it’s done compliantly and the rules in your area are followed. The steady service and parts volume is usually better handled with transparent interchange-plus pricing than with a surcharge.

Keep reading on automotive payments and what you pay

See What Your Service Drive Is Really Paying

Send Brookside one recent statement and we’ll calculate your true effective rate by department, show you where a store-wide flat rate is overcharging the service and parts volume, and flag whether your big-ticket card payments should be surcharged or capped. No switch required to find out. Learn more about payment processing consumer protections from the CFPB.

Get Your Dealership Rate ReviewedNo obligation • No pressure • Response within one business day