Trucking Payment Processing: Why the Card Is the Smallest Part

Trucking Payment Processing: Why the Card Is the Smallest Part

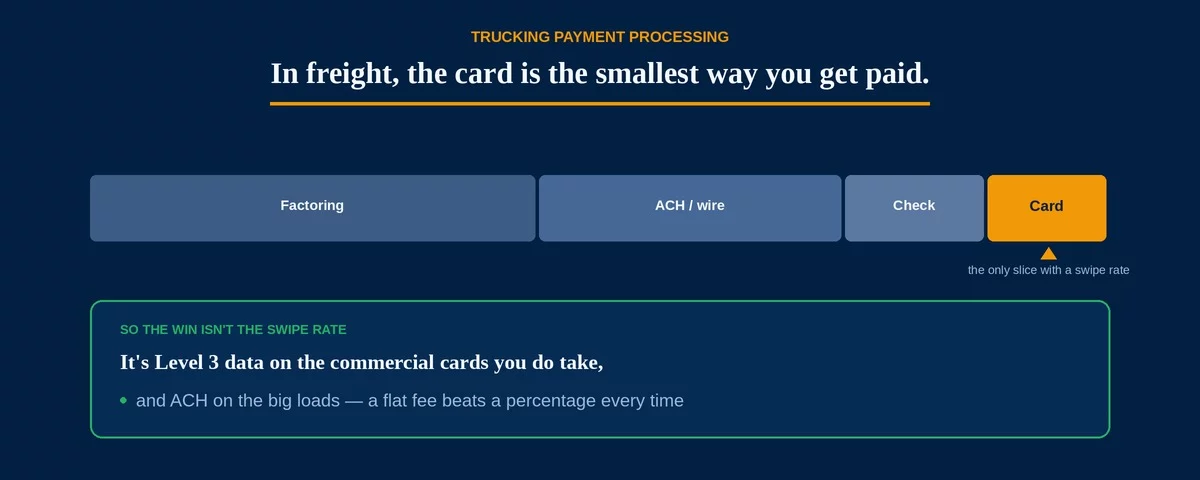

Most guides to trucking payment processing start with the swipe rate. That is the wrong end of the truck. In freight, the card is the smallest way you get paid — the money arrives mostly through factoring, ACH, wire, and paper checks, with cards handling a thin slice at the edges. So when a carrier tries to cut costs by shopping the card rate alone, they are optimizing the smallest line and ignoring the largest. The savings in trucking payment processing are real, but they live in a different place than a retailer’s would.

That does not mean the card slice is free money you can ignore. It means the levers are specific: the commercial cards you do take are almost always overpaying, and the largest payments should rarely be on a card at all. Get those two right and the rest takes care of itself.

A load settles through factoring or quick-pay for immediate cash, ACH or wire for direct-pay shippers, a check for the old-school accounts, and a card only for the smaller brokers, accessorial reimbursements, and driver expenses. The card is where the swipe rate lives — and it is the least of your volume.

Small Doesn’t Mean Free — the Card You Take Is Usually a Commercial One

When a broker or shipper pays a carrier by card, it is almost never a consumer card. It is a corporate or purchasing card, and those carry the most expensive interchange the networks publish — unless the transaction is submitted with the extra data the network wants. Most trucking payment processing setups never send that data, so every commercial card silently downgrades to the top rate. On a single $3,000 load paid by card, the difference between a qualified commercial rate and a downgrade is real money, and it repeats on every card load all year.

The second leak is the processor’s pricing model. A flat-rate app charges the same percentage on a $4,000 freight payment that it charges on a $12 coffee, which is fine for the coffee and punishing for the freight. That is why trucking payment processing rewards a transparent model far more than a retailer’s would — your average card ticket is large, and a percentage on a large ticket is where flat pricing quietly takes the most.

A purchasing card without line-item detail drops to the network’s most expensive tier. Multiply that gap by every card-paid load in a year and it is one of the largest avoidable costs in trucking payment processing — hidden precisely because the card slice looks too small to matter.

A Percentage on a $5,000 Load Is a Choice, Not a Rule

Here is the part that surprises carriers: the largest payments should usually not touch a card at all. A shipper who pays a $5,000 invoice by card costs you around $145 at a typical rate. The same payment by ACH costs a flat fee measured in cents. Nothing about the money requires the card rail — it is habit, not necessity. Steering your largest direct-pay accounts to ACH is the single biggest lever in trucking payment processing, and it is one you control.

- Paid by card at roughly 2.9%: about $145 in fees

- Paid by ACH: a flat fee, often under a dollar

- Difference on one load: about $144 — and freight runs on thin margins

This is the same logic the wholesale and manufacturing guides describe for large B2B invoices — freight is simply another business billing other businesses on big tickets, where a flat percentage does the most damage and the bank rail does the least.

How to Reduce What Trucking Payment Processing Actually Costs

Because the card is the small slice, the fix is not a heroic rate negotiation. It is three targeted moves, each aimed at where the money really leaks.

One: get on interchange-plus, not flat-rate. Your card tickets are large, so a transparent interchange-plus rate — the network’s real cost plus a visible margin — beats a blended percentage by the most on exactly the payments you take. This is the foundation the rest sits on.

Two: pass Level 2 and Level 3 data on commercial cards. The corporate and purchasing cards brokers use qualify for materially lower interchange when the transaction carries line-item detail. It is worth understanding how Level 2 and Level 3 data work before you pick a processor, because most trucking setups never turn it on and pay the downgrade every time.

Three: route the big loads to ACH. Give your direct-pay shippers a simple ACH option and reserve the card for the smaller, faster payments where speed is worth the fee. A flat bank-rail fee beats a percentage on every five-figure load.

A carrier running a few hundred thousand a year in card-paid loads typically leaves thousands on the table under a flat rate with no Level 3 and no ACH path. Fixing the model, qualifying the commercial cards, and moving the big loads to ACH recovers most of it — without changing a single thing about how the freight moves.

If you factor invoices, that fee is a financing cost, not a processing cost, and it is negotiated differently. But the loads you keep in-house and collect yourself still run through your merchant account — so the card and ACH levers above apply to every dollar you are not factoring.

Frequently Asked Questions

The ticket size and the payment mix. Freight is paid mostly by factoring, ACH, and check, with large card tickets at the edges — so a flat percentage and un-qualified commercial cards cost far more than they would in retail. The lever is the card and ACH strategy, not a lower swipe rate on tiny sales.

Yes, for the payments where speed matters — smaller brokers, accessorials, and quick-pay. Just price those cards on interchange-plus with Level 3 data, and steer your largest direct-pay accounts to ACH so a percentage never lands on a five-figure load.

Yes. The commercial and purchasing cards brokers use qualify for lower B2B interchange when line-item detail is submitted. Most trucking payment processing accounts never send it, so those cards downgrade to the most expensive tier — enabling Level 3 is the biggest single saving on the cards you take.

The B2B neighbors, the pricing model, and the two rails that do the work

Send Us One Statement. We’ll Show You the Markup.

If your carrier takes any load payments by card and the rate hasn’t been looked at in a while, there is a good chance you’re overpaying on the commercial cards and paying a percentage on loads that should run by ACH. Send Brookside one recent processing statement and a sample of how your largest accounts pay, and we’ll calculate your real effective rate, flag whether Level 2/3 data is being passed, and show you which payments belong on ACH instead of a card. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day