Convenience Store Payment Processing: Price the Swipe, Not the Sale

The Corner Store Lives and Dies on the Fixed Fee

A convenience store rings up a thousand tiny sales a day — a $2.50 soda, a $4 bag of chips, a $1.25 coffee. On tickets that small, the part of the processing cost that hurts isn’t the percentage rate; it’s the fixed per-transaction fee, the flat dime-or-fifteen-cents that lands on every single swipe no matter how small the sale. Do that a thousand times a day and the math turns brutal. That’s the whole story of convenience store payment processing: the rate barely matters, the per-swipe fee is everything, and the stores that survive it have built their pricing around exactly that fact.

It’s why the corner store is the most cash-discount-driven business in all of retail — the card-price/cash-price sign by the register isn’t a gimmick, it’s survival math. The same reality runs the urban bodega, the gas-station c-store, and the rural one-stop. Get convenience store payment processing wrong and the fixed fee quietly eats a few points of a margin that was already razor-thin. Get it right and you keep what’s yours on every $2 sale.

On a $2.50 Sale, the Per-Swipe Fee Is the Enemy — Not the Rate

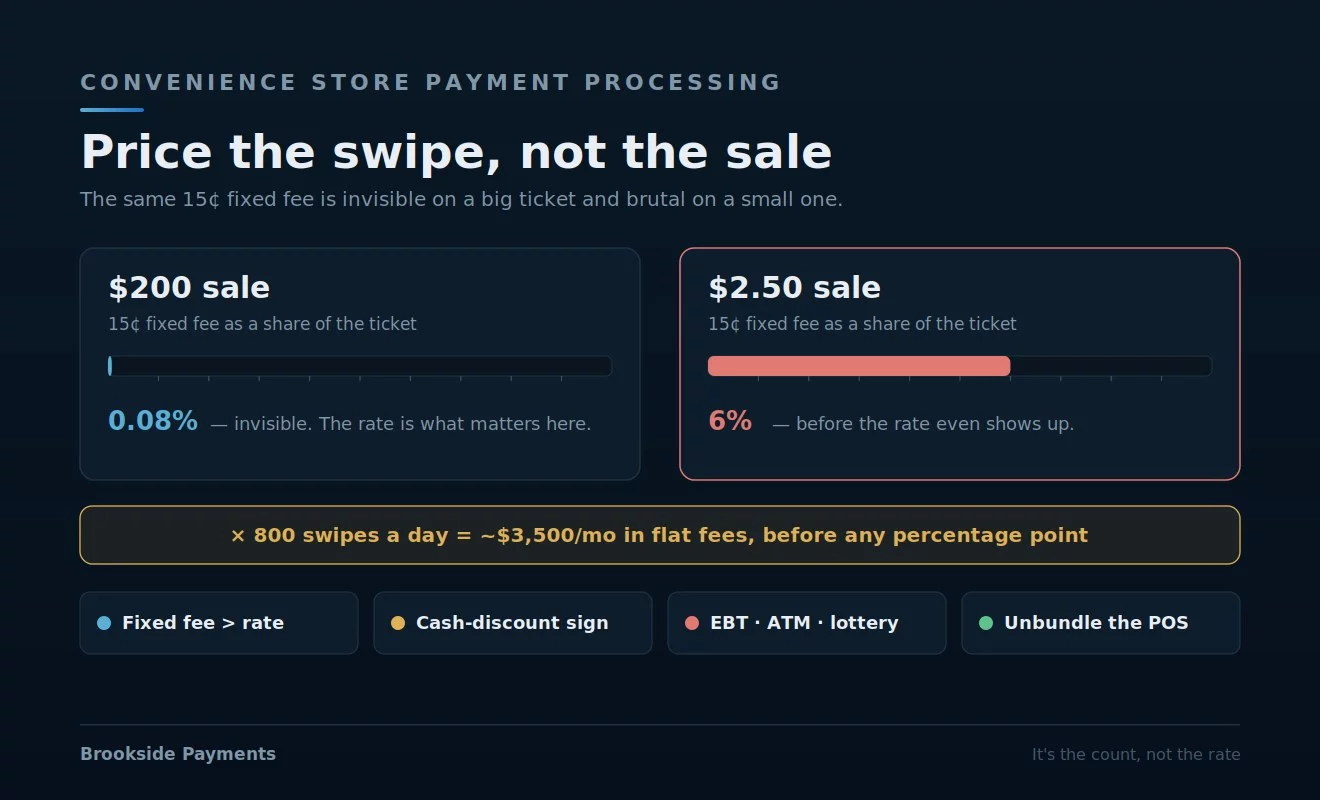

Processing cost has two parts: a percentage of the sale, and a flat fee per transaction. On a $200 sale the flat fee is a rounding error and the percentage is what matters. At a c-store counter it’s the exact opposite. On a $2.50 sale, a fifteen-cent per-transaction fee is six percent before the percentage rate even shows up — and you can’t out-negotiate a flat fee with a better rate. This is the part of convenience store payment processing that generic “we’ll lower your rate” pitches completely miss: your problem isn’t the rate, it’s the count.

Multiply it out and it stops being subtle. A store doing 800 card transactions a day at fifteen cents each is paying $120 a day — over $3,500 a month — in flat fees alone, before a single percentage point. That’s why a convenience store merchant account has to be judged on the per-transaction fee first and the rate second, the reverse of how most merchants are sold. The fee on the small ticket is the line that decides whether the card is helping you or quietly bleeding you.

On micro-tickets the flat per-transaction fee dwarfs the percentage. A fifteen-cent fee on a $2.50 sale is 6% on its own. Shaving a tenth of a point off the rate does almost nothing; cutting or offsetting the per-swipe fee does everything. Price the per-transaction fee first — it’s the number that actually runs convenience store payment processing.

The Card-Price / Cash-Price Sign Is Survival, Not a Gimmick

Walk into any corner store and you’ll see it: one price for cash, a slightly higher one for card. That’s a cash-discount or dual-pricing program, and convenience stores adopted it before almost anyone because the fixed-fee math forced their hand. When you can’t make a $2 sale work at card cost, you post the card price and give the cash buyer a discount — the processing cost moves to the customer who chose the more expensive way to pay, and your margin on the small ticket survives. This structure is the legal backbone of convenience store payment processing, valid in all fifty states and it’s the backbone of convenience store payment processing done well.

The nuance worth getting right is the difference between a true cash discount and a dual-pricing or surcharge setup — they look identical at the register but follow different rules, and getting the structure and signage right is what keeps it compliant and dispute-free. A clean convenience store credit card processing setup builds the program in correctly from the start rather than bolting a surcharge on and hoping. The sign is doing real financial work; it deserves to be set up properly.

The fixed fee on a tiny ticket can’t be beaten by rate alone, so the structure that works is moving the card cost to the card-paying customer through a posted cash-vs-card price. It’s legal in all fifty states. The catch is running it as a properly built cash-discount or dual-pricing program — not an improvised surcharge — so it stays compliant and the charges don’t get disputed.

A C-Store Account Has to Handle More Than Card Swipes

A convenience store isn’t just selling chips for a card. The register handles EBT/SNAP for eligible food, an ATM in the corner, lottery payouts, money orders, and age-restricted tobacco and alcohol — each with its own rules, its own equipment, and in EBT’s case its own federal authorization (you can’t accept SNAP without an FNS permit). None of that is “card processing” in the narrow sense, but all of it shapes which account, terminal, and POS a store actually needs. That breadth is what makes convenience store payment processing its own animal rather than generic retail.

The practical risk is mismatch: a store gets sold a slick card setup that ignores the rest of the counter, and now EBT runs on a separate clunky terminal, the ATM isn’t integrated, and lottery reconciliation is a nightly headache. The reason to treat bodega payment processing as its own category is to size the whole counter — cards, EBT, cash, ATM, the age-restricted prompts — as one system, not a card reader with everything else taped around it.

Convenience store payment processing has to account for a whole counter: EBT/SNAP (which needs an FNS permit), ATM, lottery, money orders, and age-restricted sales all live at the same register and all shape your equipment and account. A setup that solves card swipes but ignores the rest leaves you running a separate terminal for EBT and reconciling lottery by hand. The counter is one system — spec it that way.

Your POS Vendor’s Bundled Rate Is Where the Margin Hides

Convenience-store POS systems are powerful — they handle age verification, lottery, EBT, and inventory — and they almost always come with processing baked in at a rate the POS company sets. That bundling is convenient, and it’s also where the markup hides: the per-transaction fee and rate are buried inside a monthly POS bill, hard to see and harder to compare. For a business where the per-swipe fee is the whole game, a marked-up bundled rate is the most expensive kind of invisible. Good convenience store payment processing pulls the processing apart from the POS so you can actually see and price it.

That doesn’t always mean changing your POS — it means knowing your real per-transaction cost inside the bundle, and whether you can route processing to a better-priced account while keeping the system you like. The hardware can stay; the processing underneath it is negotiable far more often than the POS rep lets on. Unbundling the cost is usually the single biggest lever in corner store payment processing, precisely because the bundle was built to keep it hidden.

C-store POS systems bundle processing at a rate the vendor sets, hiding the per-transaction fee inside a monthly bill. On micro-tickets that’s the most expensive place for convenience store payment processing to let it hide. You can usually keep the POS and still move the processing to a better-priced account — but only once you’ve pulled the real per-swipe cost out of the bundle and looked at it.

Price the Swipe, Not the Sale

Convenience stores don’t get beaten by a high rate — they get beaten by a flat fee on a tiny ticket, multiplied by a thousand a day. Convenience store payment processing done well starts where the money actually leaks: price the per-transaction fee first, build the cash-discount or dual-pricing program in cleanly so the card cost lands where it should, size the whole counter — EBT, ATM, lottery, age-restricted — as one system, and pull the processing out of the POS bundle so you can see it. Bodega, gas-station c-store, or rural one-stop, it’s the same counter and the same math. Get those right and every $2 sale keeps the few cents that were always supposed to be yours.

Frequently Asked Questions

Good convenience store payment processing starts from one fact: usually it isn’t the rate, it’s the fixed per-transaction fee. On a $2.50 sale a flat fifteen-cent fee is already 6%, and a busy store rings up hundreds or thousands of those a day, so the flat fees pile up far faster than the percentage ever does. The fix is to evaluate the per-transaction fee first and offset it with a cash-discount program, not to chase a slightly lower rate.

Yes, and it sits at the center of convenience store payment processing: that’s a cash-discount or dual-pricing program, and it’s legal in all fifty states. You post the card price and give cash buyers a discount, which moves the card cost to the customer who chose to pay by card. The important part is building it as a proper, compliant program with the right signage rather than improvising a surcharge, so the charges hold up and don’t get disputed.

You need a separate federal authorization — an FNS permit from the USDA — to accept SNAP, and it runs alongside your card processing rather than through it. That’s part of why convenience store payment processing is best sized as a whole counter: cards, EBT, ATM, and lottery each have their own rails, and a good setup makes them work together instead of leaving EBT stranded on its own terminal.

Keep reading on tiny tickets and what you pay

Find the Fixed Fee Hiding in Your Counter

Send Brookside one recent statement and we’ll show you your true per-transaction cost across your card volume, what a cash-discount or dual-pricing program would actually save a store at your ticket size, and whether your processing is marked up inside a POS bundle. That’s convenience store payment processing sized to the whole counter — cards, EBT, ATM, lottery — not just the card reader. No switch required to find out. You can also review card payment protections from the CFPB.

Get Your Counter ReviewedNo obligation • No pressure • Response within one business day