How to Choose an ACH Processor: 7 Things to Compare

First, Know What You’re Actually Comparing

Figuring out how to choose an ACH processor matters more than most businesses expect, because once you have decided to accept bank payments, the providers all look interchangeable — and they are not. The rail underneath is the same for everyone. The differences that cost you money live one layer up: the pricing model, the funding speed, the risk terms, and the contract.

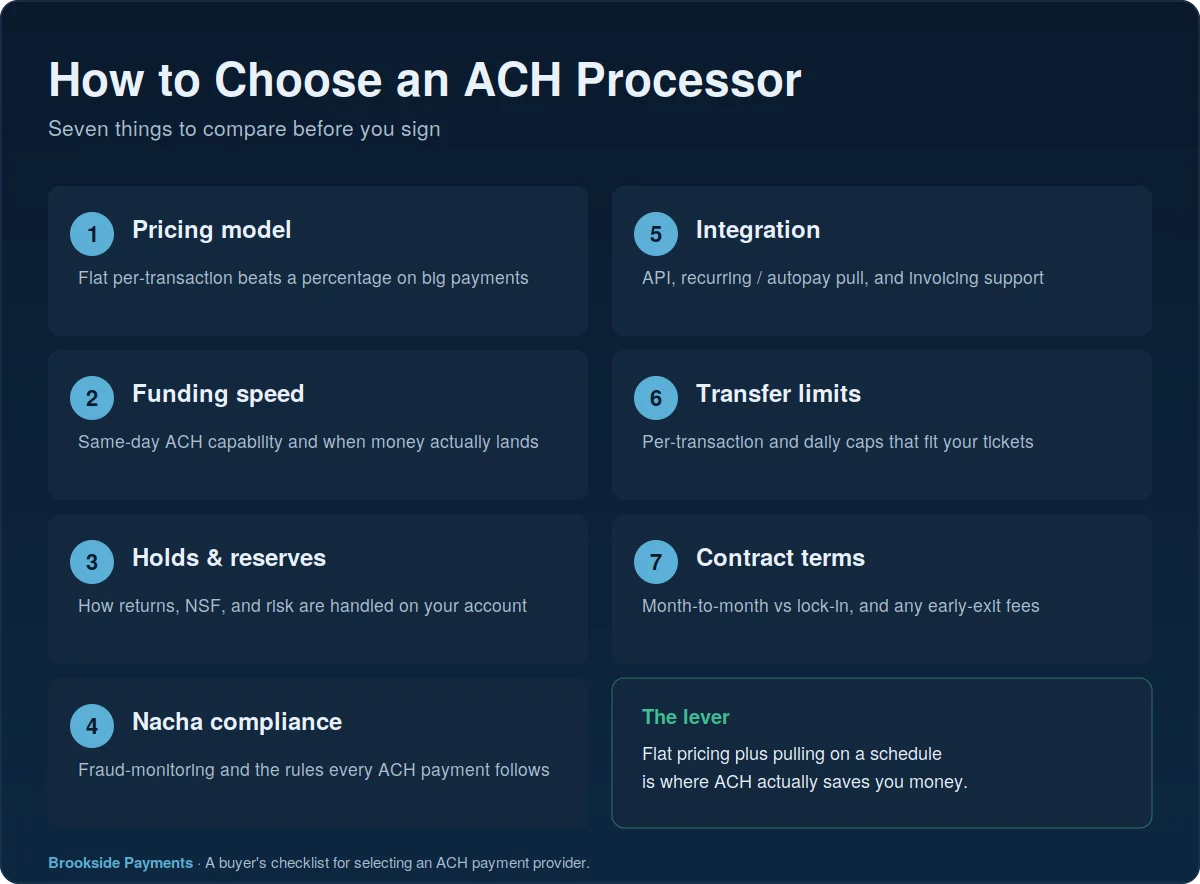

It helps to know what you are even choosing among. Most ACH providers are one of a few types: your business bank, a card processor that bolts ACH onto its existing service, an ACH-specialist provider, or a software platform that resells someone else’s processing. Same Nacha network underneath, very different cost and terms on top. Here are the seven things to compare before you sign.

Every ACH processor moves money over the same bank network governed by Nacha rules. So you are not really shopping for a faster or “better” rail — you are shopping for the pricing, the funding speed, the risk handling, and the support wrapped around it.

Pricing Model: Flat Beats Percentage on Real Money

This is the single biggest cost difference between providers, and it is the first question to ask. ACH pricing comes in two shapes: a flat per-transaction fee (a fixed amount per payment, regardless of size) or a percentage of the amount (sometimes with a cap). On a $25 payment the two barely differ. On a $20,000 invoice, a 0.75% rate is $150 — for the exact same bank transfer that costs the processor a few cents.

If your payments are large or recurring, flat pricing almost always wins, and a percentage model quietly scales your cost with the size of every payment. While you are comparing, watch for the add-ons that hide the real rate: monthly minimums, batch fees, and return or NSF fees. The clean way to compare is on your own numbers — see what you actually pay in ACH processing fees.

Percentage pricing on high-ticket ACH is how businesses end up paying card-like money for a cents-cost rail. A processor quoting “just 1%” sounds cheap until you run it against a $50,000 supplier payment — that is $500 for a transfer a flat-fee provider would move for under a dollar.

Funding Speed: Standard, Same-Day, or Held

Standard ACH settles in one to three business days. Same-day ACH compresses that into same-day windows for an added fee, which is worth it when timing matters and skippable when it does not. Ask which the processor supports and what same-day costs — then ask the question most businesses forget: when does the processor actually release the funds to you? Some add a day of their own hold on top of the rail’s timing, which means two providers quoting the same same-day label can land your money a full day apart. Get the real end-to-end timing in writing, not just the rail’s headline speed.

If settlement speed is the whole reason you are shopping, weigh it against the alternatives before committing. Faster card deposits may solve the same problem — see next-day funding — and for payments that truly need to clear in seconds, the instant rails are a different tool entirely, covered in instant payments vs ACH.

Holds, Reserves, and Nacha Compliance

ACH carries return risk — insufficient funds, closed accounts, and disputed or unauthorized debits all come back to the processor, and ultimately to you. How a provider manages that risk shapes your experience. Some impose a reserve, hold a portion of your funds, or cap your volume, especially in the first months. Ask three things directly: how returns are handled, whether there is a reserve, and what specifically triggers a hold.

Then ask about compliance. Nacha writes the ACH rulebook, and a 2026 Nacha fraud-monitoring rule now applies to every ACH sender. A serious processor has that monitoring built in rather than bolted on after a problem — it is a fair proxy for how seriously they take the rest of the rules.

A reserve or rolling hold is not automatically a dealbreaker, but vague language is. If the contract lets the processor hold your money at its discretion with no defined trigger or release window, you want that spelled out before money is moving, not after.

Integration, Limits, and the Contract

Match the processor to how you will actually collect. If you bill the same customers repeatedly, the whole point of ACH is its ability to pull on a schedule — so recurring and autopay support has to be solid, not an afterthought. Decide whether you need a developer API, a hosted payment page, invoicing, or all three, and confirm the provider does that one well rather than everything poorly.

Check the limits next: per-transaction and daily caps that comfortably clear your largest tickets, not just your average ones. Finally, read the contract. Good ACH processing is month-to-month. A multi-year lock-in with an early-termination fee is a red flag for a service this commoditized — if a provider asks you to sign one, ask why the rail itself is not enough to keep you.

How to Choose an ACH Processor: The Short Checklist

Run every provider through the same seven questions, in this order: flat or percentage pricing; standard or same-day funding (and when they release it); how returns, reserves, and holds work; whether Nacha fraud monitoring is built in; whether the integration fits how you collect; whether the limits clear your biggest payments; and whether the contract is month-to-month. The provider that answers those cleanly is usually the right one — the brand name matters far less than the terms.

And keep the goal in view. The reason to get ACH right is not the rail itself; it is the cost. Most businesses overpay simply by running everything through cards out of habit, when a flat-priced ACH provider would move their recurring and B2B payments for cents. That is why how to choose an ACH processor really comes down to terms over brand name: the cheapest rail in payments only saves you money if the provider sitting on top of it is priced to let it.

Flat per-transaction pricing plus pulling on a schedule is the combination that beats cards. Get those two right and the processor you pick will pay for itself on the first large invoice you stop running over a card.

Frequently Asked Questions

Many payment processors also handle ACH, so the labels overlap. An ACH processor specifically moves bank-to-bank payments over the Nacha network rather than the card networks. What matters when you compare is the pricing model and the terms, not whether the provider calls itself an “ACH processor” or a “payment processor.”

Flat per-transaction pricing almost always wins once your payments get large, because a percentage model scales your cost with the size of every transfer even though the bank rail costs the same regardless. Compare both against your actual ticket sizes — the bigger and more frequent your payments, the more flat pricing saves.

Usually not. ACH processing is commoditized enough that strong providers offer month-to-month terms. A multi-year contract with an early-termination fee is worth questioning — if the pricing and service are competitive, the provider should not need a lock-in to keep you.

Send Us Your Setup. We’ll Tell You If You’re on the Wrong Pricing Model.

If you are paying a percentage on ACH payments — or running large invoices over cards out of habit — you are very likely overpaying. Send Brookside your current ACH pricing or a recent statement and we’ll run the flat-versus-percentage math against your actual ticket sizes and tell you what a better-fit processor would cost. The review takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Check My ACH PricingNo obligation • No pressure • Response within one business day

See what a statement review looks like →