Reduce Acumatica Payment Processing Fees Without Leaving Acumatica

Reduce Acumatica Payment Processing Fees Without Leaving Acumatica

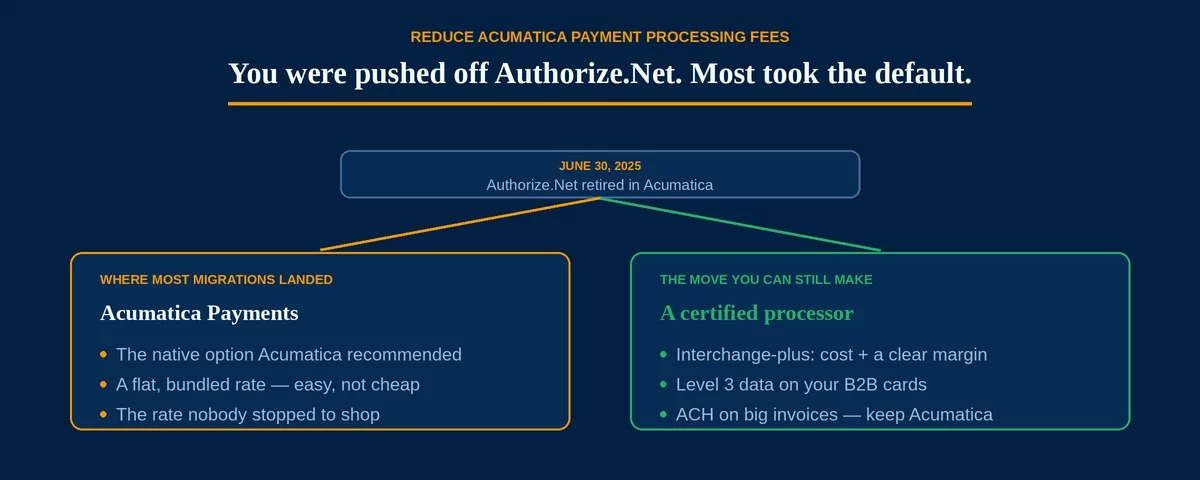

Acumatica runs the business — financials, invoicing, accounts receivable. Then, with the 2025 R1 release, Acumatica retired the Authorize.Net plug-in and ended support for it, which forced every shop still on that gateway to migrate. Most took the path of least resistance: Acumatica Payments, the native, flat-rate option Acumatica itself recommended. That switch was also the one moment you were guaranteed to look at payments — and almost nobody used it to shop the rate. That is why you can still reduce Acumatica payment processing fees without leaving the platform: the door the migration opened has not closed.

Here is the part most teams miss: the platform integrates with a range of certified processors, not just the native default. You keep every workflow and change only the economics underneath. The money is in the flat rate nobody compared, and in the card data your transactions do or do not carry.

When Acumatica deprecated the Authorize.Net plug-in in 2025, shops had to move to the native Acumatica Payments or to a certified third-party processor. Native was the easy default — but the marketplace of certified processors is where an interchange-plus rate lives. Both keep you inside the platform; only one is priced to be cheap.

Why the Flat-Rate Default Rarely Gets Questioned

A forced migration is stressful, and the native option is the safe-looking choice — recommended, quick to enable, one point of support. So most shops flipped to Acumatica Payments, confirmed that transactions posted cleanly, and moved on. Once payments reconcile, the rate stops being a question, and switching again feels like a project you just finished. So a flat rate chosen under deadline pressure quietly becomes the most expensive line on the statement, and re-shopping it is the first step to reduce Acumatica payment processing fees.

A bundled, one-size rate is built to be easy, not cheap. It folds the network’s real cost into a single percentage you cannot see inside, which is harmless on small tickets and expensive on large ones. That blend is the gap you are closing when you set out to reduce Acumatica payment processing fees.

The migration was mandatory; taking the native flat rate was not. A rate picked to get off Authorize.Net quickly, and never compared afterward, is a rate that only ever costs you more — most on your largest B2B invoices.

Large B2B Invoices Carry the Most Markup

Its base runs deep in cloud-ERP mid-market — distributors, manufacturers, and project-based services that bill other businesses on large invoices and net terms. That is precisely where a flat percentage does the most damage. A $40,000 invoice on a 2.9% flat rate costs $1,160 in fees; the same invoice on interchange-plus pricing, with Level 2 and Level 3 data attached, can land far lower, because qualifying a commercial card unlocks the B2B interchange built for exactly these transactions.

- Flat rate at 2.9%: $1,160 in fees

- Interchange-plus with Level 3 data, roughly 1.9% all-in: about $760

- Difference on a single invoice: about $400 — illustrative, and the real figure moves with card mix and margin

Most setups never pass Level 2/3 data, so commercial cards drop to the most expensive interchange the network offers. Closing that gap across a year of invoices is the single biggest way to reduce Acumatica payment processing fees — and it is the same problem the manufacturing and wholesale guides describe; the ERP is simply where it lives for cloud-run shops.

How to Reduce Acumatica Payment Processing Fees

Because you have already migrated once, the fix is the easy part — a reconfiguration, not a project. There are three moves that reduce Acumatica payment processing fees, and the platform supports all three without disrupting a workflow.

One: place a certified interchange-plus processor. The platform’s marketplace includes processors that integrate as cleanly as the native option but price at the network’s real cost plus a transparent margin, so payments still post inside the platform exactly as they do today — only the rate changes.

Two: turn on Level 2 and Level 3 data. Submitting line-item detail qualifies your commercial-card transactions for materially lower B2B interchange. It is the most valuable lever and the one most setups skip, so it is worth understanding how Level 2 and Level 3 data work before you choose a processor.

Three: route your largest invoices to ACH. The platform handles ACH payments alongside cards, and a flat-dollar bank-rail fee beats a percentage on a five- or six-figure invoice.

A shop running a few million a year in card volume typically leaves five figures on the table under a native flat rate. A certified interchange-plus processor, Level 3 data, and an ACH path for the biggest invoices recover most of it — and your team keeps working entirely inside Acumatica.

Moving from the native processor to a certified one is routine but not instant. Confirm the processor is certified for your version, test before going live, and keep the old setup active long enough to settle pending authorizations and process refunds on transactions it already handled.

Running a different platform changes the details. If you are on NetSuite or SAP Business One, the story is similar with different tools; if you are on QuickBooks rather than a full ERP, start with reduce QuickBooks payment processing fees instead.

Frequently Asked Questions

Yes. Acumatica integrates with a range of certified processors, so you can keep the ERP and every workflow your team knows, and simply place a cheaper interchange-plus processor in place of the native default. You change the rate and the data, not the ERP — the cleanest way to reduce Acumatica payment processing fees.

Acumatica retired the Authorize.Net plug-in with its 2025 R1 release and ended support for it, so shops had to move to the native Acumatica Payments or a certified third-party processor. If you took the native flat rate under deadline, that same migration is your opening to move to interchange-plus instead.

Yes, with a processor that supports it. The platform can submit the line-item detail that qualifies commercial cards for lower interchange — most setups simply never turn it on. Enabling it is the single biggest saving on large B2B invoices.

The vertical behind Acumatica, the ERP siblings, and the pricing model that fixes them

Send Us One Statement. We’ll Show You the Markup.

If you moved to Acumatica Payments when Authorize.Net was retired and haven’t looked at the rate since, there is a good chance you can reduce Acumatica payment processing fees on every large invoice. Send Brookside one recent processing statement and a sample invoice, and we’ll calculate your real effective rate, flag whether Level 2/3 data is being passed, and show you what a certified interchange-plus processor would save — without changing how Acumatica works. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day