Capital One’s Discover Merger Just Raised Your Debit Interchange. Here’s the Math.

On May 18, 2025, Capital One closed its $35.3 billion acquisition of Discover Financial Services. The combined company is now the sixth-largest U.S. bank by assets and one of the three largest credit card issuers in the country.

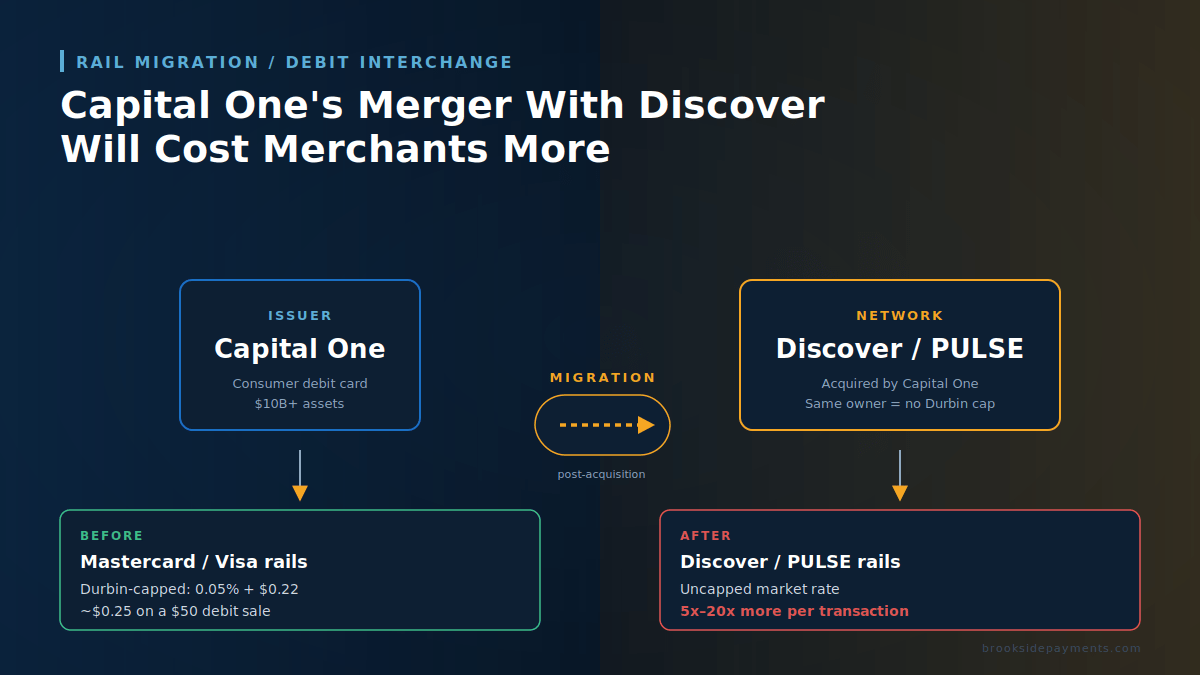

The headlines focused on the size of the deal. The thing that affects merchants is smaller, quieter, and already showing up on processing statements: Capital One is moving its debit card portfolio off the Mastercard network and onto the Discover and PULSE networks it now owns. The migration started in June 2025 and is progressing gradually card-by-card. The result is that Capital One Discover debit interchange — the new combined-network rate — is replacing the older Mastercard debit rate on a growing share of transactions.

The reason this matters is structural. Discover is exempt from the Durbin Amendment debit interchange caps. Mastercard and Visa are not. By moving its debit cards onto a network it owns, Capital One stops being a “covered issuer” for those transactions and starts charging merchants the higher unregulated debit rate. For some merchants, that rate is roughly three times what they paid before. For low-ticket and card-not-present transactions, the multiple is higher.

This post explains exactly what changed, how to spot the new charges on your statement, and what your realistic options are. The short version is that there is no fix you can apply unilaterally to the Capital One Discover debit interchange rate. The longer version is worth understanding, because the same playbook may extend to credit cards in 2027.

Why Owning the Network Changes the Capital One Discover Debit Interchange Math

U.S. debit card interchange has been governed since 2011 by Regulation II, the Federal Reserve rule that implemented the Durbin Amendment to the Dodd-Frank Act. Reg II caps debit card interchange for issuers with more than $10 billion in assets at 0.05% of the transaction value plus a fixed amount of $0.21, with a $0.01 fraud-prevention adjustment for compliant issuers — an effective cap of $0.22 plus 0.05% per transaction. Until the merger, that cap is what set Capital One Discover debit interchange policy across the entire Capital One debit portfolio.

The cap was designed to address the same complaint merchants had been raising for years: debit interchange is a per-swipe tax that bears no relation to the cost of authorizing the transaction. A debit card draws funds directly from a customer’s bank account. There is no credit risk, no float, no rewards program funded by the swipe fee. The cap was Congress’s attempt to acknowledge that and force interchange on debit toward something closer to actual cost.

The cap has one structural exemption, and that exemption is the entire reason this acquisition happened.

The Durbin cap applies only to debit cards processed through “four-party” networks — networks where the issuing bank, the acquiring bank, the merchant, and the network are four distinct entities (Visa and Mastercard). It does not apply to “three-party” or closed-loop networks, where the network and the issuing bank are the same entity. American Express and Discover are the two consumer-facing closed-loop networks in the U.S.

Before the merger, Capital One was a covered issuer. Its debit cards ran on Mastercard rails. Every Capital One debit transaction was capped at the Durbin rate, and Capital One Discover debit interchange did not yet exist as a category.

After the merger, Capital One owns Discover. When a Capital One debit card is reissued onto the Discover network, the same physical card now runs through a closed-loop system where Capital One is both the issuer and the network operator. The four-party structure that triggered the Durbin cap no longer exists for that transaction. The transaction is now exempt — and Capital One can charge the unregulated Capital One Discover debit interchange rate instead.

The migration is the entire economic point of the acquisition. Capital One disclosed to investors that shifting its debit volume to Discover would generate over $1 billion in annual interchange revenue. That money has to come from somewhere. It comes from merchants.

Capital One Discover Debit Interchange: Old Rate vs. New Rate

The “before” rate is the Durbin-regulated debit cap. The “after” rate — the new Capital One Discover debit interchange figure — is one of three Discover unregulated debit interchange categories, depending on how the transaction is processed.

0.05% + $0.22

Applies to all debit cards from issuers with $10B+ in assets, when processed through Visa or Mastercard.

1.10% + $0.16

card-present transactions

Higher rates apply to recurring billing and card-not-present.

The full Discover unregulated debit interchange table breaks into three main categories most merchants will see:

| Transaction Type | Discover Rate | Cost on a $50 Sale |

|---|---|---|

| Card-present (in-store, dipped or tapped) | 1.10% + $0.16 | $0.71 |

| Recurring billing (MCCs 4814 and 4899 — telecom, utilities) | 1.20% + $0.05 | $0.65 |

| Card-not-present (keyed, e-commerce) | 1.75% + $0.20 | $1.08 |

Compare those to the Durbin cap on the same $50 sale: $0.245. Card-present transactions on the new Capital One Discover debit interchange rate cost the merchant 2.9 times more. Card-not-present transactions cost 4.4 times more. The multiplier looks worse on smaller transactions because the per-transaction component dominates — a $5 debit sale that used to cost $0.245 now costs $0.215 card-present (slightly less, actually) but $0.288 recurring or $0.288 card-not-present, and the per-item math compounds across thousands of monthly transactions.

Optimized Payments, the industry consultancy tracking this most closely, modeled a hypothetical merchant doing $1 billion in annual card volume with 12% Capital One share. At full migration, that merchant faces an annual interchange increase of approximately $72,000 — a 26% rise in their Capital One Discover debit interchange costs. For most independent businesses processing $50,000 to $500,000 a month, the impact scales down proportionally but remains real money.

Recognizing Capital One Discover Debit Interchange Charges on Your Statement

The migration is rolling, not all-at-once. As of late 2025, Capital One had begun moving debit volume but had not completed the full portfolio. eMarketer reported that the migration has hit “snags” and is proceeding more slowly than originally projected. That means a merchant accepting Capital One debit cards may be seeing two different rates on the same statement right now — some transactions still on Mastercard at the Durbin cap, others showing the new Capital One Discover debit interchange rate.

Three signals to look for on your next processing statement:

1. New Discover BINs that did not appear in your historical data. The first six digits of a card number identify the issuer and network. As Capital One reissues cards onto Discover, those cards carry Discover BINs — even though Capital One is still the bank behind them. Specifically, BIN ranges 601141, 601144, and 601146 are absorbing the bulk of the migrated Capital One debit volume. Your processor’s reporting tools should let you filter by BIN range. New volume on those Discover BINs is the migration showing up.

2. Discover, Diners Club, or PULSE logos on physical Capital One debit cards. Any of those three brand marks indicate the card is now running on the Discover network. Capital One is reissuing cards as customers’ existing cards expire or are replaced for other reasons.

3. New interchange line items in the Discover section of your statement labeled with rates above 1%. Most merchants are familiar with Discover credit interchange but rarely see Discover debit at all because the volume was historically tiny. If a “Discover Debit Card-Present” or “Discover PSL Recurring Payments” line suddenly appears with material volume, you are looking at migrated Capital One cards being billed at the new Capital One Discover debit interchange rate.

This is one of the situations where the pricing model on your merchant account dictates whether you can see what is happening at all. On a flat-rate or tiered processing plan, the new rate is buried inside a blended number you cannot decompose. On interchange-plus pricing, every interchange category appears as its own line — which means the migrated volume is visible to you the moment it hits your statement. This is exactly the scenario where the transparency of interchange-plus pays for itself.

What You Can And Cannot Do About the Capital One Discover Debit Interchange Rate

The honest answer is that there is no merchant-side workaround that prevents the Capital One Discover debit interchange rate from applying. The interchange categories are set by the network, not by your processor or your contract. Once a Capital One debit card has been reissued on the Discover network, every transaction on that card runs at the Discover rate. You cannot decline Capital One debit cards specifically, you cannot route them differently, and you cannot negotiate the underlying interchange.

What you can control is everything around the rate. Three actions that matter when Capital One Discover debit interchange volume starts showing up on your statement:

Get on interchange-plus pricing if you are not already.

This is the single most important action. If you cannot see the line items, you cannot quantify the impact, and you cannot make any informed decision about the rest of your processing setup. Interchange-plus exposes the actual interchange categories on every statement. Flat-rate and tiered pricing both hide them. Compare your current pricing model here.

Audit your processor markup.

The interchange itself is non-negotiable, but your processor’s markup on top of it is. If interchange is going up because of forces outside your control, the margin your processor takes on every transaction is the only place there is room to recover. A statement review identifies whether your effective markup is competitive — see how to calculate your effective rate for the math.

For high-volume recurring billers: model the impact before you set 2027 pricing.

The rate increase hits recurring billing categories hardest. If you operate under MCCs 4814 (telecom) or 4899 (cable, satellite, streaming) or any subscription-heavy model, the cost of accepting a Capital One debit card on a recurring transaction is now meaningfully higher than it was. That belongs in any pricing decision you are making for the next 12 months.

What is not a viable option: refusing Discover. Discover acceptance is now table stakes — 99% of U.S. merchants who accept Visa or Mastercard also accept Discover, and the Department of Justice required Capital One to maintain the Discover network for at least five years as a merger condition. Telling customers you no longer accept their card to avoid the Capital One Discover debit interchange fee structure means losing the sale entirely.

Why The Capital One Discover Merger Is The Beginning, Not The End

The debit migration is the first wave of Capital One Discover debit interchange repricing. Capital One has publicly stated it intends to move portions of its credit card portfolio onto the Discover network as well, with completion targeted for 2027. That is a much larger pool of volume — Capital One is one of the top three credit card issuers in the country — and the same structural logic applies. Credit card interchange is not Durbin-capped at all, but moving credit volume from Visa or Mastercard onto Discover gives Capital One leverage in the interchange-fee negotiations it conducts as an issuer with the two larger networks. The Federal Trade Commission and merchant trade groups have flagged this as a coordination risk.

The political response to the merger has been fragmented. Senator Elizabeth Warren urged the Department of Justice to challenge the deal in May 2025; the DOJ declined. The Merchants Payments Coalition and National Retail Federation publicly opposed the merger. Senator Dick Durbin and Senator Roger Marshall continue to push the Credit Card Competition Act, which would force large issuers to enable a second network on every card — a different problem from Discover ownership but the same underlying market dynamic.

None of that legislation has passed. The acquisition closed. The migration is happening. The question for any merchant accepting card payments is no longer whether the Capital One Discover debit interchange rate will change but how much of your debit volume will be on Capital One cards by the time it does.

The companion to this post — the Visa Level 2 sunset on April 17 — covered an unrelated regulatory event with similar downstream effects on B2B merchants. Both happened in the same month. Both went mostly unannounced by the processors that should have flagged them. The pattern is consistent: network rule changes increasingly happen without merchant-facing notice, and the only defense is a pricing structure transparent enough to surface them.

Frequently Asked Questions

Discover is exempt from the Durbin Amendment debit interchange caps that apply to Visa and Mastercard. Capital One’s $35.3 billion acquisition of Discover Financial Services closed May 18, 2025, and Capital One has been moving its debit card portfolio off the Mastercard network onto the Discover and PULSE networks it now owns. Once a Capital One debit card moves to Discover, the transaction runs at unregulated rates — typically 1.10% + $0.16 card-present, 1.75% + $0.20 card-not-present — instead of the Durbin cap of 0.05% + $0.22. On a $50 sale, that is $0.71 versus $0.245 for card-present, or $1.08 versus $0.245 for card-not-present. The structural change happened at the regulatory level, not at your processor.

Three signals on your processing statement. New Discover BINs that did not appear in your historical data — the first six digits of a card number identify the issuer and network, and as Capital One reissues cards onto Discover, those cards carry Discover BINs even though Capital One is still the bank. Specifically, BIN ranges 601141, 601144, and 601146 are absorbing the bulk of the migrated Capital One debit volume. Discover, Diners Club, or PULSE logos on physical Capital One debit cards. New interchange line items on your statement labeled with Discover unregulated debit categories rather than Mastercard regulated debit. The migration is gradual, so you may see the same Capital One cardholder running at the old Mastercard rate one month and the new Discover rate the next.

No. The interchange categories are set by the network, not by your processor or your contract. Once a Capital One debit card has been reissued on the Discover network, every transaction on that card runs at the Discover rate. You cannot decline Capital One debit cards specifically, you cannot route them differently, and you cannot negotiate the underlying interchange. What you can control is everything around the rate — your pricing model, your processor markup, and how visible the impact is on your statement.

Capital One has publicly stated it intends to move portions of its credit card portfolio onto the Discover network as well, with completion targeted for 2027. That is a much larger pool of volume — Capital One is one of the top three credit card issuers in the country. Credit card interchange is not Durbin-capped at all, but moving credit volume from Visa or Mastercard onto Discover gives Capital One leverage in interchange-fee negotiations it conducts with the two larger networks. The debit migration that started in 2025 is the first wave; the credit migration is the larger one still ahead. Merchants will see this pattern repeat over the next two to three years.

Three actions matter. Get on interchange-plus pricing if you are not already — the single most important step, because flat-rate and tiered pricing both hide the line items, and you cannot quantify the impact or make informed decisions if you cannot see the categories. Audit your processor markup — the interchange itself is non-negotiable, but the markup your processor charges on top of interchange is fully negotiable, and a competing quote at renewal is the leverage that moves it. Track your effective rate monthly — total fees divided by total card volume; if the number has crept up over the last six months, the migration is showing up, and the visible drift is what gives you the basis to act on it.

Read Next

Find Out What Is Already Hitting Your Statement

If your processing statement does not break out interchange line by line, the Capital One migration is invisible to you — but you are paying for it. A free statement review surfaces every interchange category, identifies migrated volume, and quantifies what your effective rate has done in the last six months. No commitment, no obligation.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day