Discover merchant settlement claim window timeline showing May 18 2026 deadline

Source: discovermerchantsettlement.com · CAPP Inc. v. Discover Financial Services, Case No. 1:23-cv-04676 (N.D. Ill.)

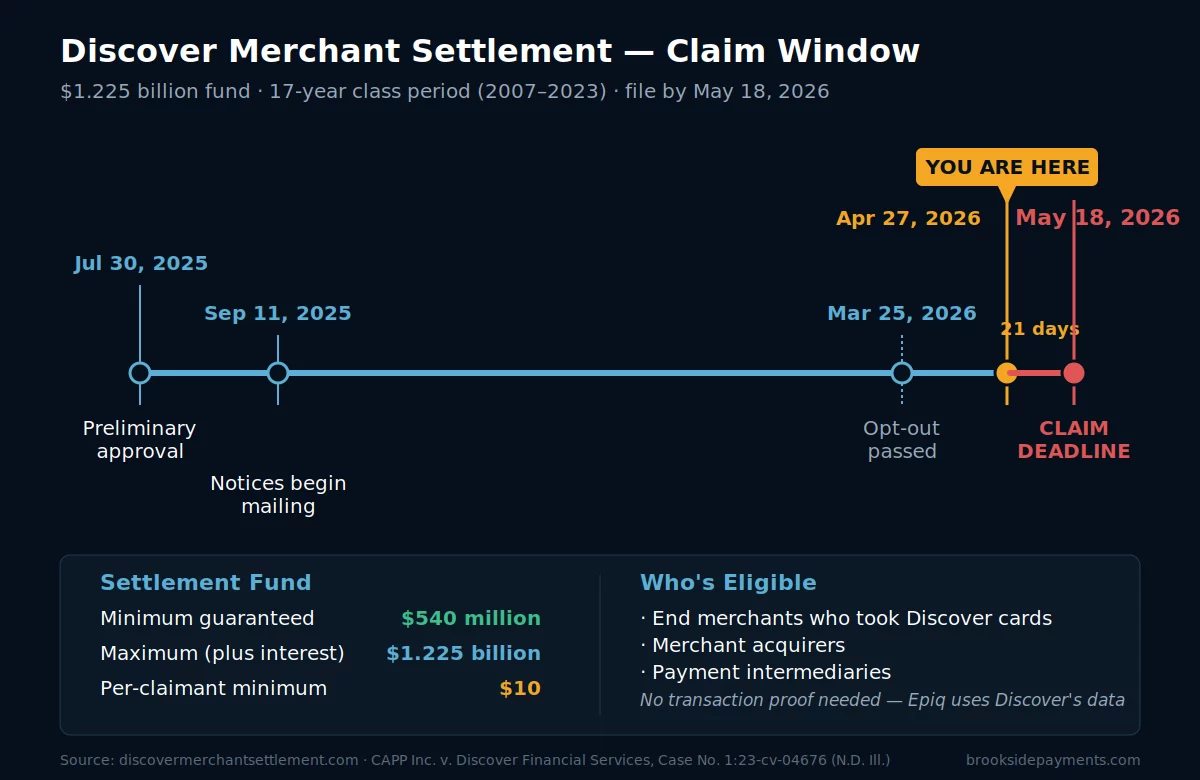

The Discover merchant settlement closed on May 18, 2026. The $1.225 billion fund is now being distributed to the merchants who filed. This page is a retrospective — what the settlement was, who qualified, what filers should expect next, and why the bigger Visa-Mastercard settlement now in court approval is the more important story for any merchant still on a card-accepting business.

Discover Financial Services spent 17 years quietly classifying about five million consumer credit cards as commercial — and charging merchants the higher interchange that came with the label. When the Discover merchant settlement closed on May 18, 2026, the $1.225 billion fund earmarked to repay them was waiting on filings most merchants never made. The window is closed. The lesson is not.

Discover Financial Services agreed to pay between $540 million and $1.225 billion plus interest to resolve allegations that it misclassified roughly five million consumer credit cards as commercial cards over a 17-year stretch. Commercial cards carry higher interchange fees than consumer cards. The complaint alleged the misclassification cost merchants approximately one percent extra on every affected transaction. Discover has not admitted wrongdoing, but federal regulators imposed a separate $250 million in civil money penalties — $150 million from the FDIC, $100 million from the Federal Reserve — covering the same conduct.

This post walks through what the settlement is, who qualifies, what merchants will actually get paid, and the five-minute filing process. The deadline is real. After May 18, 2026, the door closes and any unclaimed share gets distributed pro rata among merchants who did file. Filing costs nothing.

What This Settlement Is — And Why It Exists

For 17 years, Discover’s records classified certain consumer credit cards — specifically rewards, premium, and premium plus tiers — as commercial cards. Commercial card interchange runs at roughly 2.4 percent. Consumer card interchange runs closer to 1.4 percent. Every time a consumer swiped one of those misclassified cards at your business, your processor passed the higher commercial interchange through to your statement. You paid the commercial rate on a transaction that should have been the consumer rate.

The disclosure came from inside Discover. In a July 2023 earnings call, then-CEO Roger Hochschild publicly acknowledged the misclassification issue. He resigned weeks later. By July 2025, three related class action lawsuits — CAPP, Inc. v. Discover Financial Services (Case No. 1:23-cv-04676), Lemmo’s Pizzeria, LLC v. Discover Financial Services, and Support Animal Holdings, LLC v. Discover Financial Services — had been consolidated and the U.S. District Court for the Northern District of Illinois granted preliminary approval to the settlement.

The Discover merchant settlement is the largest of three parallel actions against Discover for the same conduct. Federal regulators acted independently. The FDIC issued three orders against Discover Bank, including the $150 million civil money penalty. The Federal Reserve Board issued its own enforcement order with a $100 million penalty. The size of those penalties is the tell. When two federal agencies layer a quarter-billion in fines on top of a billion-dollar restitution fund, the regulator’s view of the conduct is not ambiguous.

If a $1,000 sale ran on a misclassified card, the difference between commercial interchange and consumer interchange was roughly $10 on that single transaction. Over a 17-year window, across millions of transactions, the cumulative overcharge across the merchant base was reportedly more than $1 billion — the figure the regulators arrived at independently.

Who Qualifies for the Discover Merchant Settlement

The settlement class is broad. The Discover merchant settlement covers three categories of business, all defined by the qualifying period of January 1, 2007 through December 31, 2023:

End merchants — any individual or business that accepted Discover-issued credit cards directly from a customer in exchange for goods or services during the qualifying window. This is the category most small business owners will fall into. The settlement administrator further subdivides end merchants into four sub-types (indirect, inactive direct, managed active direct, unmanaged active direct), but the practical answer for nearly every Brookside reader is straightforward: if you took Discover cards, you qualify.

Merchant acquirers — businesses that had a formal agreement with Discover to facilitate card transactions. Most readers of this post are not in this category; it covers processors and acquiring banks themselves.

Payment intermediaries — businesses that processed Discover transactions on behalf of other merchants without being end merchants or acquirers themselves. Software platforms with embedded payments, ISO operations, and certain payfacs may fall here.

One detail worth surfacing: if your business has closed, you may still qualify under the Discover merchant settlement as long as it operated during the class window and accepted Discover cards. The legal entity needs to be in a position to receive payment, but the business does not need to be currently operating.

The opt-out deadline was March 25, 2026 — that window has passed. Anyone who did not opt out before that date is automatically a member of the settlement class. Most class members must still file a claim form to receive payment. A small subset of “unmanaged active direct end merchants” will receive payment automatically, but that category is narrow. If you’re reading this post, assume you have to file.

What You’ll Actually Get Paid

The Discover merchant settlement establishes a guaranteed minimum total payout to class members of $540 million and a maximum of $1.225 billion plus interest. Within those bounds, individual payments are calculated pro rata based on the estimated overcharge tied to each Discover merchant identifier, or MID, associated with your business.

The mechanics matter for setting expectations. Every approved class member is guaranteed at least $10 — even merchants whose calculated overcharge was tiny or whose Discover volume was minimal during the class window. If the total of all those base payments would exceed $50 million in aggregate, the per-claimant base is reduced pro rata so the cap holds. On the other end, if total claim payments come in below $540 million, every payment increases proportionally until the floor is met. The fund pays out a minimum of $540 million regardless of how many merchants file.

Industry estimates suggest roughly 96 percent of class action settlement funds historically go unclaimed. The fewer merchants who file, the larger each filer’s share — within the floor and ceiling. Your share goes up when other merchants don’t file. Filing matters more than it appears.

How will you know what you’re owed? After the May 18 deadline closes, the Settlement Administrator (Epiq Class Action and Claims Solutions) will issue a Claim Determination Notice with your specific Allocated MID Amount calculated from Discover’s own transaction records. You’ll have an opportunity to challenge the allocation if your records show different volume than what Discover reports. Payments are issued by check or ACH transfer, your choice during filing.

Payment timing: approximately 240 days after the court grants final approval. The final approval hearing is scheduled for May 20, 2026. Realistic disbursement window is late 2026 to early 2027.

How the Filing Worked — and What Filers Should Expect Next

Filing the Discover merchant settlement claim is free, takes most merchants under five minutes online, and does not require receipts, statements, or transaction records. Epiq calculates payment from Discover’s own data. You’re not proving how much you spent — Discover already knows.

If you received a notice in the mail or by email: the notice contains a Claimant ID and PIN. Go to discovermerchantsettlement.com, click Submit a Claim, register an account, enter your Claimant ID and PIN, and follow the prompts. Most merchants will be done within five minutes.

If you didn’t receive a notice but accepted Discover cards during the class period: you can still file. Notices were mailed on a rolling basis through April 30, 2026 — many eligible merchants never received one because Discover’s records of historical merchants are incomplete. Go to the same site, register, and use your business Taxpayer Identification Number (EIN, SSN, or ITIN) instead of a Claimant ID. The Administrator will pull your MID associations from Discover’s records.

If you prefer mail: download the claim form from the Documents tab, complete it, and send to: Discover Card Merchant Class Action Settlement Administrator, c/o Epiq Class Action, P.O. Box 2497, Portland, OR 97208-2497. Mail submissions must be postmarked by May 18, 2026. Online is faster and easier — recommend the portal unless you have a specific reason to file by mail.

If you operate under multiple TINs or DBAs: the system organizes records by TIN. If your business has changed legal entity over the years, you may need to file separately for each TIN that accepted Discover cards. After filing one, you can add additional Claimant IDs to your existing portal account from the My Claims page.

If your business is a payment intermediary: there’s a specialty team for this category at 1-877-535-8067 or DirectServices@DiscoverMerchantSettlement.com. Payment intermediaries had their own February 25, 2026 milestone for certain documentation; verify with the specialty team whether you have remaining steps.

Once you submit the claim, you cannot withdraw it — only opt out, which is no longer an option since March 25 passed. Submit when you’re ready, and the Administrator will follow up if anything else is needed.

Why This Matters Beyond the Check

The Discover merchant settlement is, in one frame, a one-time recovery opportunity tied to a specific 17-year billing error at one network. That’s the headline. But the structural lesson the Discover merchant settlement leaves behind — the one merchants should sit with after they file — is more durable.

For 17 years, every Discover transaction at every business that took the cards carried a roughly one percent overcharge that nobody noticed. Not the merchants. Not the merchants’ processors. Not the merchants’ bookkeepers. Not the merchants’ accountants. The error showed up on every monthly statement throughout the entire class period and read as normal interchange. It did not get flagged because the entire system between the merchant and the network is designed to make any single transaction’s interchange line look like every other transaction’s interchange line. There is no path on a standard processing statement for a merchant to verify that a Discover-card swipe actually carried the consumer rate it should have carried instead of the commercial rate it was billed at.

What broke the silence was a CEO publicly disclosing the issue on an earnings call. Not a merchant catching it. Not an auditor. Not a processor. A class action followed. Federal regulators followed the class action. None of those mechanisms would have moved without the original disclosure — and the original disclosure happened only because the misclassification had become large enough to require disclosure as a financial item to investors.

The next opaque billing pattern is already running on someone’s statement somewhere. The lesson isn’t that Discover is uniquely dishonest. The lesson is that the structure of merchant statements makes anomalies invisible by design — and the only practical defense is having someone read the statement who knows what each line is supposed to be doing.

Frequently Asked Questions

You can still file. Go to discovermerchantsettlement.com, click Submit a Claim, and register using your business Taxpayer Identification Number (EIN, SSN, or ITIN) instead of a Claimant ID. The Settlement Administrator will pull your MID associations from Discover’s records. Notices were mailed on a rolling basis through April 30, 2026, so many eligible merchants never received one. The deadline still applies — May 18, 2026.

Yes, if the business operated during the class window (January 1, 2007 through December 31, 2023) and accepted Discover cards. The legal entity needs to be in a position to receive payment, but the business does not need to be currently operating. File using the historical TIN.

No. Epiq calculates each merchant’s overcharge from Discover’s own MID data. Most claimants file with only basic business identification (legal name, DBA, taxpayer ID, contact info). If the Administrator needs anything beyond that — typically a W-9 — they’ll request it after you file. If your portal shows MIDs that don’t match your records, you can upload statements to request a correction.

The Settlement Closed. The Next One Is Already in Motion.

The Discover settlement is done. The bigger merchant-network settlement is not. Visa and Mastercard’s proposed $38 billion deal — which would trim the combined average effective credit interchange rate by 0.10% for five years, cap standard consumer card rates at 1.25% for eight, and expand surcharge rights — moved to Judge Brodie for preliminary approval in early 2026 and faces active objections from the National Restaurant Association, NACS, Walmart, and Hugo Boss (Payments Dive). The window to understand what your statement looks like before any of that lands is now. We can read your current processing statement in fifteen minutes and tell you what every line is doing. Free. No commitment to switch.

Get Your Free Statement ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →