Reduce Fishbowl Payment Processing Fees Without Leaving Fishbowl

Reduce Fishbowl Payment Processing Fees Without Leaving Fishbowl

Fishbowl runs the floor — inventory, manufacturing, warehouse, and the sales orders that turn into invoices. When you started taking cards, Fishbowl Payments was right there at signup, so you switched it on. The rate looked reasonable, got approved once, and has priced every card payment since. That is how small manufacturers end up overpaying — and why you can reduce Fishbowl payment processing fees without leaving the software.

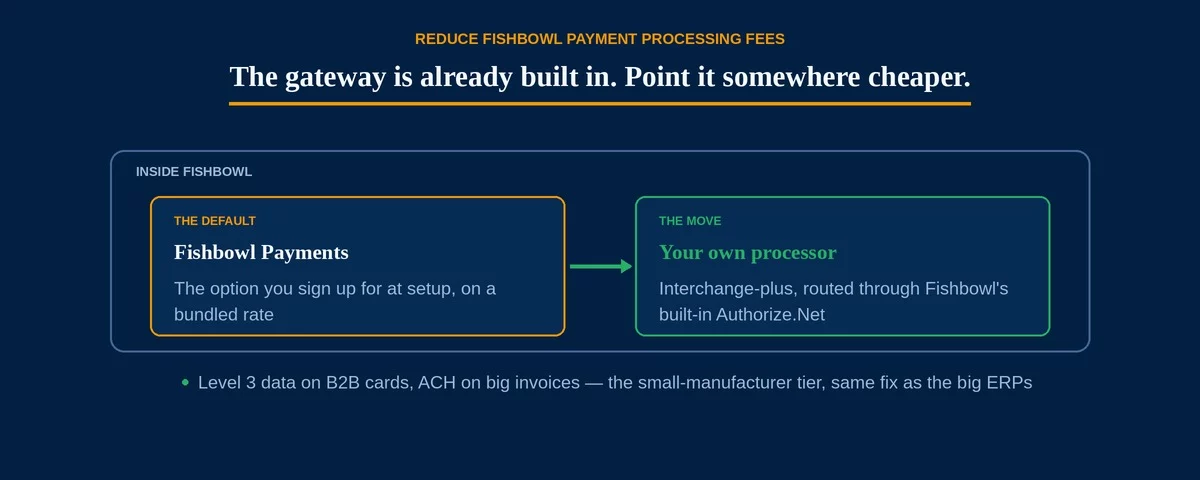

Here is the lever most shops never use: a payment gateway is already built into the software, and it can point at a processor of your choosing. You keep every workflow and change only the economics underneath. The money is in the bundled rate Fishbowl Payments quietly set, and in the card data your transactions do or do not carry.

Fishbowl Payments is the native option promoted at signup. But Authorize.Net is built directly into Fishbowl’s interface, and other gateways connect through it too — so the path to your own, cheaper processor is already inside the software you run.

Why the Fishbowl Payments Rate Rarely Gets Questioned

The convenience is real, and so is the cost. Fishbowl Payments is the path of least resistance: it is native, quick to enable, and marketed on simplicity. Once payments post cleanly against sales orders, the rate stops being a question. Most shops never revisit it — switching feels like a project, so a bundled rate that was fine at signup quietly becomes the most expensive line on the statement — and re-examining it is the first step to reduce Fishbowl payment processing fees.

A bundled, one-size rate is built to be easy, not cheap. It folds the network’s real cost into a single percentage you cannot see inside, which is harmless on small tickets and expensive on large ones. That blend is the gap you are closing when you set out to reduce Fishbowl payment processing fees.

Native and simple is not the same as competitive. Accepting the payment option promoted at signup saves an afternoon and can cost thousands a year afterward — because the rate stops being examined the moment payments reconcile cleanly.

Even Small-Shop Invoices Carry the Markup

Its market is small and mid-size manufacturers, wholesalers, and warehouses — businesses that still send large B2B orders even without a full enterprise ERP. That is precisely where a flat percentage does the most damage. A $40,000 order on a 2.9% bundled rate costs $1,160 in fees; the same order on interchange-plus pricing, with Level 2 and Level 3 data attached, can land far lower, because qualifying a commercial card unlocks the B2B interchange built for exactly these transactions.

- Flat bundled rate at 2.9%: $1,160 in fees

- Interchange-plus with Level 3 data, roughly 1.9% all-in: about $760

- Difference on a single order: about $400 — illustrative, and the real figure moves with card mix and margin

Most setups never pass Level 2/3 data, so commercial cards drop to the most expensive interchange the network offers. Closing that gap across a year of orders is the single biggest way to reduce Fishbowl payment processing fees — and it is the same problem the manufacturing and wholesale guides describe, scaled to the smaller-shop tier.

How to Reduce Fishbowl Payment Processing Fees

Because a gateway is already built into the software, the fix is a reconfiguration, not a migration. There are three moves that reduce Fishbowl payment processing fees, and the software supports all three without disrupting a workflow.

One: route the built-in gateway to your own processor. You point Fishbowl’s Authorize.Net connection at an interchange-plus processor instead of the bundled default, so transactions still post inside the software exactly as today — only the rate changes.

Two: turn on Level 2 and Level 3 data. Submitting line-item detail qualifies your commercial-card transactions for materially lower B2B interchange. It is the most valuable lever and the one most setups skip, so it is worth understanding how Level 2 and Level 3 data work before you choose a processor.

Three: route your largest orders to ACH. The software handles ACH payments alongside cards, and a flat-dollar bank-rail fee beats a percentage on a five-figure order.

A shop running a million or more a year in card volume typically leaves thousands on the table under a bundled rate. Your own interchange-plus processor, Level 3 data, and an ACH path for the biggest orders recover most of it — and your team keeps working entirely inside Fishbowl.

Re-pointing the built-in gateway to a new processor is routine but not instant. Test the connection before going live, and keep the old processor active long enough to settle pending authorizations and process refunds on transactions it already handled.

The software often sits alongside QuickBooks, so if your accounting runs there too, see reduce QuickBooks payment processing fees. And if you graduate to a full ERP, the same fix applies on NetSuite, SAP Business One, Epicor, Sage, and Acumatica.

Frequently Asked Questions

Yes. A payment gateway is already built into the software, so you can point it at a cheaper interchange-plus processor while every sales order, invoice, and reconciliation workflow stays exactly the same. You change the rate and the data, not the software — which is how you reduce Fishbowl payment processing fees without a migration.

No. Fishbowl Payments is the native default, but Authorize.Net is built into its interface and other gateways connect through it, so you can bring your own processor and merchant account. That is what makes the rate yours to change.

Yes, with a processor that supports it. The software can submit the line-item detail that qualifies commercial cards for lower interchange — most setups simply never turn it on. Enabling it is the single biggest saving on large B2B orders.

The vertical behind Fishbowl, the ERP siblings, and the pricing model that fixes them

Send Us One Fishbowl Statement. We’ll Show You the Markup.

If your payments run through Fishbowl Payments and the rate hasn’t been looked at since setup, there is a good chance you can reduce Fishbowl payment processing fees on every large order. Send Brookside one recent processing statement and a sample invoice, and we’ll calculate your real effective rate, flag whether Level 2/3 data is being passed, and show you what your own interchange-plus processor through its built-in gateway would save — without changing how Fishbowl works. The math takes us about fifteen minutes. Learn more about payment processing consumer protections from the CFPB.

Send Your Statement for a Free ReviewNo obligation • No pressure • Response within one business day