Approved Friday, Funded Wednesday: When Card Sales Actually Reach Your Bank

Next-Day Funding Is the Gap Between a Sale and the Money in Your Account

Next day funding sounds like a technicality until the week your card sales and your payroll run cross paths. A customer taps a card, the terminal says approved, the sale is done — and somewhere in the back of your mind the money is already in the bank. It isn’t. Approval and funding are two different events, often separated by several days, and the gap between them is where a profitable business can still come up short on a Monday morning.

This is the part of payments that almost no one explains at signup, because it doesn’t show up as a fee or a rate. It shows up as timing — and for any business that runs payroll on a fixed calendar, timing is its own kind of cost.

How the Money Actually Moves

When a card is approved, all that’s happened is an authorization — the issuing bank has confirmed the funds exist and put a hold on them. No money has moved. The money moves later, in two steps most owners never see: you close out the day’s sales in a batch, and your processor submits that batch for settlement. Funds then land in your account on the processor’s funding schedule.

For most U.S. merchants that schedule runs one to three business days from the batch. The single biggest variable you control is the daily cutoff time: every processor sets a deadline — often late afternoon, sometimes as late as the evening — and a batch closed before it funds on the next cycle, while a batch closed after it rolls into the following day’s. Closing the batch (or auto-batching) at the same time every day, ahead of that cutoff, is what makes funding predictable instead of a guess. Whether each batch even carries a separate batch fee is a different question — but the timing is set by when the batch closes, not by what it costs.

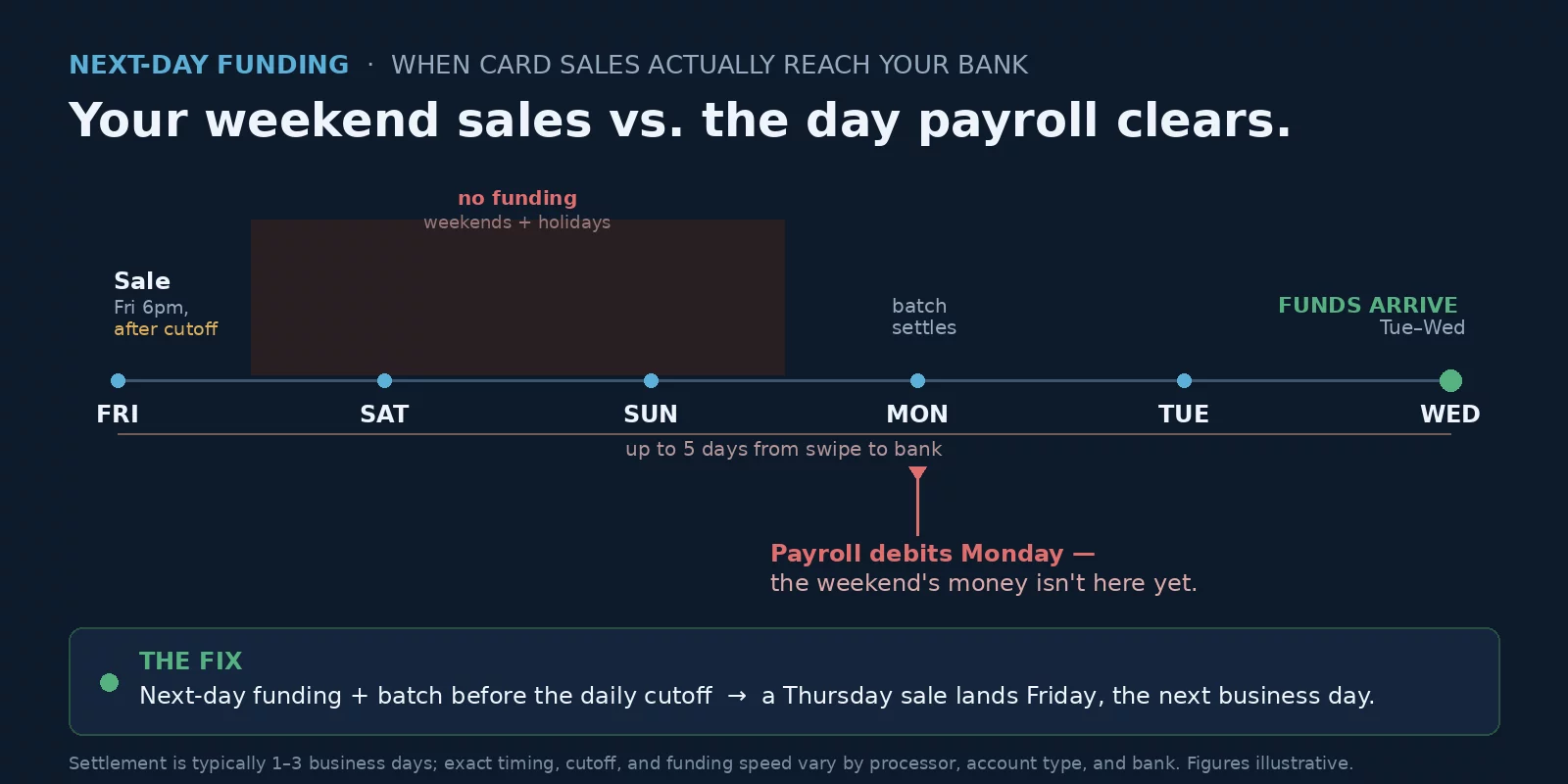

Weekends, Holidays, and the Cutoff

Standard funding happens on business days only. Weekends and federal holidays aren’t skipped so much as paused: a batch that would have funded Saturday simply waits for Monday, and a deposit scheduled on a holiday slides to the next business day. Stack that on top of a missed cutoff and the gap widens fast.

A sale rung up Friday night, after the cutoff, doesn’t batch until the next business day — Monday. From there it’s another business day or two to settle. A weekend’s worth of card revenue you earned on Friday and Saturday can sit untouchable until Tuesday or Wednesday, even on an account that “funds next day.”

Friday’s Sales Don’t Always Cover Monday’s Payroll

Here’s where the timing turns into a real problem. Payroll doesn’t wait for your funding schedule. A payroll run is an ACH debit that hits your account on a fixed day — and if your provider pulls it Monday or Tuesday while your strong weekend is still in the settlement pipeline, you can be short on cash you have genuinely already earned. The sales happened. The money is real. It just isn’t there yet.

For a business with thin reserves, a heavy inventory reorder, or a tight payroll calendar, that lag isn’t an annoyance — it’s the difference between covering the run and watching an overdraft or a missed vendor payment. Cash flow is about when money arrives at least as much as how much, and the funding schedule on your merchant account decides the “when.”

Four Levers That Tighten the Gap

You can’t change how the banking system clears on weekends, but most of the gap is inside your control.

- Batch before the cutoff, every day. Set an automatic batch to close ahead of your processor’s deadline so a day’s sales never slip into the next cycle by accident.

- Get next-day funding as your standard — or same-day funding if payroll is tight. Many accounts default to two-day funding unless you ask. It is the right baseline; same-day funding exists for businesses that genuinely need it, sometimes for a small fee. Read the fine print: faster funding can be limited to card-present sales, subject to underwriting, or capped per transaction.

- Align the funding schedule with your payroll calendar. If payroll debits Monday, you want your highest-volume days funding before then — and a modest cash buffer to bridge the weekend gap that no funding speed fully erases.

- Keep a clean processing history. New accounts often see extra scrutiny and slower funding for the first 30 to 90 days; a steady, dispute-free record is what earns the fastest schedules.

Next-day funding (or same-day if you run payroll on a knife’s edge), an automatic daily batch that closes before the cutoff, a funding schedule that lands your big days ahead of the payroll debit, and a small buffer for the unavoidable weekend gap. None of it changes your rate — it changes when the cash is usable.

Late Funds That Aren’t About Timing

There’s a line between normal funding lag and a genuine problem. If your deposits are one to two days behind because of a weekend or a missed cutoff, that’s the calendar working as designed. If money is days or weeks late, marked “under review,” or trickling out in pieces, that’s not a funding schedule — it’s a processor holding your funds or a reserve. Holds are triggered by risk, not the clock: a sudden volume spike, a rise in chargebacks, a new account, or a higher-risk category. That’s a different conversation with a different fix, and worth recognizing early so you don’t keep waiting on money that isn’t simply “in transit.”

Speed vs. Cost — and the Number That Actually Matters

Faster funding occasionally carries a small fee or a slightly higher rate, and for a payroll-tight or inventory-heavy business that trade is usually worth making — predictable cash beats a few basis points. What’s not worth it is letting a processor sell you “fast funding” as cover for an expensive plan. Judge the whole package the way you’d judge any other: on the effective rate, with the pricing kept visible through interchange-plus pricing, so you can buy the funding speed you need without quietly overpaying for the processing itself.

Frequently Asked Questions

The approval at the terminal is instant, but that’s only an authorization — no money has moved. Funding follows after you batch the day’s sales and the processor settles them, typically one to three business days later. With next-day funding and a batch closed before your processor’s daily cutoff, the funds land the next business day; miss the cutoff and they slip a day.

Usually not. Standard funding runs on business days, so a batch closed Friday typically funds Monday, and a deposit due on a holiday moves to the next business day. A sale made Friday evening after the cutoff can take until Tuesday or Wednesday to reach your account. Some same-day funding programs do deposit seven days a week — confirm the specific schedule with your processor.

If it’s one to two days behind around a weekend, holiday, or a late batch, that’s normal timing. If money is days or weeks late, showing as “under review,” or being released in partial amounts, that points to a reserve or a funds hold driven by risk — a volume spike, chargebacks, or a new-account review — not the funding calendar. Those are different problems with different fixes.

Send Us a Statement. We’ll Check Your Funding Schedule and Cutoff.

If your deposits keep arriving after you need them, the fix is usually in the funding type, the batch cutoff, or both — and it shouldn’t cost you a rate hike to get there. Send Brookside a recent statement and we’ll tell you what funding schedule you’re actually on, whether faster funding is worth it for your payroll calendar, and what your real all-in cost is either way. The read takes about fifteen minutes. You can also review payment processing consumer protections from the CFPB.

Get a Free Funding & Statement ReviewNo obligation • No pressure • Response within one business day

See what a statement review looks like →